Key Insights

The automotive plastics market is experiencing robust growth, driven by the increasing demand for lightweight vehicles to improve fuel efficiency and reduce emissions. This trend is further amplified by the burgeoning electric vehicle (EV) sector, where plastics play a crucial role in battery casings, interior components, and other applications. The market's Compound Annual Growth Rate (CAGR) exceeding 10% indicates significant expansion potential through 2033. Key materials like polypropylene (PP), polyurethane (PU), and polyethylene (PE) dominate the market due to their cost-effectiveness, durability, and design flexibility. The automotive industry's ongoing efforts to reduce vehicle weight are fueling demand for advanced, high-performance plastics, such as polyamides (PA) and polycarbonate (PC), in structural components and safety features. Regional variations exist, with the Asia Pacific region, particularly China and India, expected to lead growth due to massive vehicle production and increasing disposable incomes. However, challenges remain, including fluctuating raw material prices and the need for sustainable and recyclable plastic solutions to meet growing environmental concerns. The shift towards electric vehicles presents both opportunities and challenges, requiring manufacturers to adapt their materials and processes to meet the specific requirements of EV technologies. Market segmentation based on material type, application (exterior, interior, under-bonnet), and vehicle type (conventional/EV) offers strategic insights for manufacturers and investors.

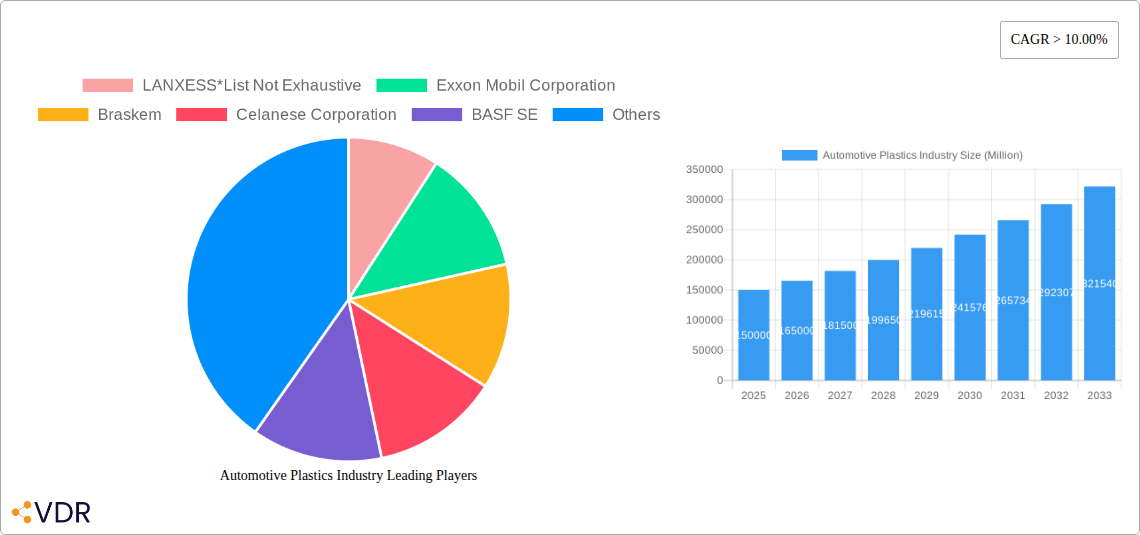

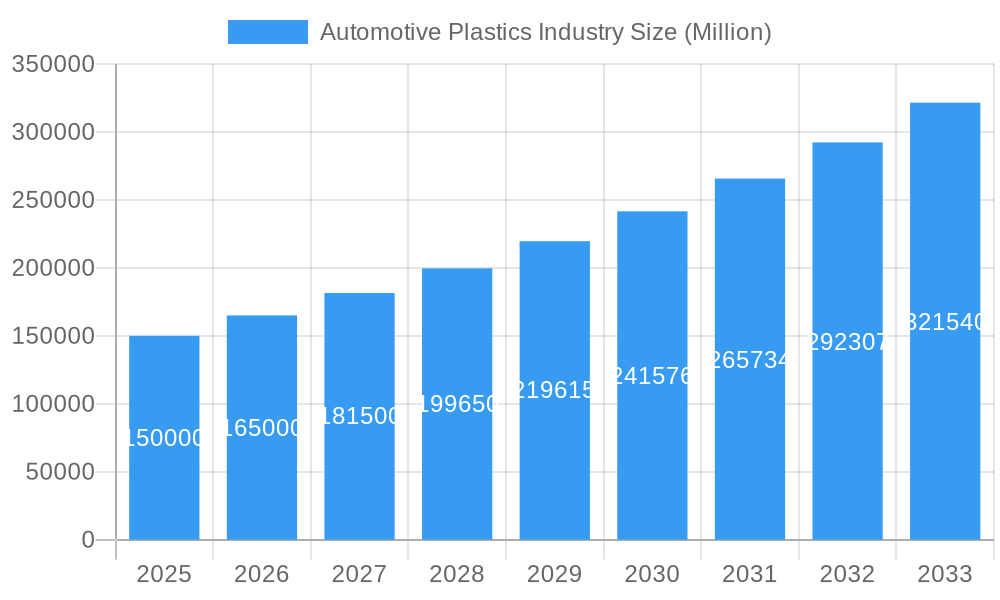

Automotive Plastics Industry Market Size (In Billion)

The competitive landscape is characterized by a mix of established chemical giants and specialized automotive suppliers. Companies like BASF, LANXESS, and ExxonMobil are major players, leveraging their extensive R&D capabilities and global reach to cater to the evolving needs of the automotive industry. The ongoing innovation in plastic materials, such as the development of bio-based and recycled plastics, is reshaping the market dynamics. The automotive plastics sector will likely continue its robust growth trajectory, driven by technological advancements and the growing focus on lightweighting and sustainability in vehicle manufacturing. Successful players will need to demonstrate a commitment to innovation, sustainable practices, and meeting the demanding requirements of both traditional and electric vehicle manufacturers.

Automotive Plastics Industry Company Market Share

Automotive Plastics Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the automotive plastics industry, encompassing market dynamics, growth trends, regional insights, product landscapes, and key players. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. This in-depth analysis is crucial for industry professionals, investors, and strategists seeking to navigate this evolving market. The report analyzes parent markets (plastics, automotive) and child markets (various polymer types, vehicle applications).

Automotive Plastics Industry Market Dynamics & Structure

The automotive plastics market is characterized by a moderately concentrated structure, with several multinational corporations holding significant market share. Key players such as LANXESS, Exxon Mobil Corporation, Braskem, Celanese Corporation, BASF SE, DSM, DuPont, Daicel Corporation, Asahi Kasei Advance Corporation, Covestro AG, and Borealis AG compete intensely, driving innovation and price competition. The market is driven by technological advancements in lightweighting materials, increasing demand for electric vehicles (EVs), and stringent regulatory frameworks focused on fuel efficiency and emissions. However, factors such as fluctuating raw material prices, supply chain disruptions, and the development of substitute materials pose significant challenges.

- Market Concentration: xx% market share held by the top 5 players in 2024.

- Technological Innovation: Focus on lightweighting, bio-based plastics, and recycled content.

- Regulatory Landscape: Stringent emission standards and fuel efficiency regulations are driving adoption of lightweight plastics.

- Competitive Substitutes: Metals and other composites represent potential substitute materials.

- M&A Activity: A moderate level of mergers and acquisitions observed in the historical period (2019-2024), with xx major deals concluded.

Automotive Plastics Industry Growth Trends & Insights

The global automotive plastics market experienced robust growth during the historical period (2019-2024), driven by increasing global vehicle production and the rising adoption of plastics in automotive applications. The market size reached xx million units in 2024, and is projected to continue its expansion with a Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, reaching xx million units by 2033. This growth is fueled by several key trends: the increasing demand for lightweight vehicles to improve fuel efficiency and reduce emissions, the growing popularity of electric vehicles, and the continuous development of advanced materials with improved properties like strength and durability. Consumer preferences for aesthetically pleasing and functional interiors also play a significant role. Technological disruptions, particularly in the area of material science and manufacturing processes, continue to shape the market landscape, driving innovation and efficiency improvements.

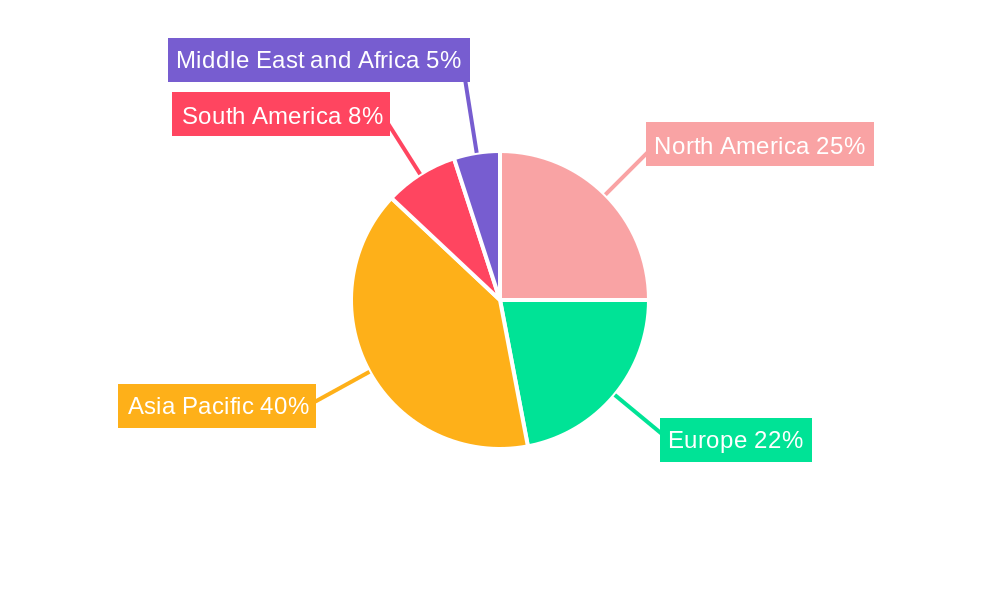

Dominant Regions, Countries, or Segments in Automotive Plastics Industry

The Asia-Pacific region dominated the automotive plastics market in 2024, accounting for xx% of the global market share, followed by North America (xx%) and Europe (xx%). This dominance is attributed to factors such as the high concentration of automotive manufacturing hubs, robust economic growth, and increasing vehicle ownership.

Within material segments, Polypropylene (PP) holds the largest market share due to its cost-effectiveness and versatility. However, Polyurethane (PU) and Polycarbonate (PC) are experiencing rapid growth due to their superior properties. The interior segment currently leads in application due to the high demand for aesthetic and functional components. However, the exterior segment shows promising growth potential due to advancements in exterior plastic components for improved aerodynamics and durability. The shift towards electric vehicles is driving demand for new materials with specific properties tailored to electric vehicle requirements.

- Key Drivers: Rapid economic growth in Asia-Pacific, increasing vehicle production, government incentives for EV adoption.

- Dominance Factors: High automotive manufacturing concentration, favorable regulatory environments, established supply chains.

- Growth Potential: Significant growth potential in developing economies, expansion into new applications for electric vehicles.

Automotive Plastics Industry Product Landscape

The automotive plastics market offers a wide array of products, including various polymer types such as polypropylene (PP), polyurethane (PU), and polycarbonate (PC), each tailored to specific applications and vehicle types. Innovations focus on enhancing performance characteristics like lightweighting, durability, and recyclability. Unique selling propositions center around improved material properties, such as enhanced impact resistance, heat resistance, and aesthetic appeal. Technological advancements include the use of recycled and bio-based materials, leading to more sustainable and environmentally friendly solutions.

Key Drivers, Barriers & Challenges in Automotive Plastics Industry

Key Drivers:

- Growing demand for lightweight vehicles to improve fuel economy and reduce emissions.

- Increasing adoption of plastics in automotive components due to cost-effectiveness and design flexibility.

- Technological advancements leading to the development of high-performance plastics with improved properties.

Challenges:

- Fluctuating raw material prices impacting profitability.

- Supply chain disruptions and logistical challenges.

- Stringent environmental regulations demanding the use of sustainable materials.

- Competition from alternative materials such as metals and composites.

Emerging Opportunities in Automotive Plastics Industry

Emerging opportunities lie in the development and adoption of bio-based and recycled plastics to meet sustainability goals. Innovative applications such as advanced lighting systems, sensor integration, and interior customization are also driving growth. Untapped markets in developing economies offer significant potential for expansion. The increasing demand for electric vehicles (EVs) presents opportunities for specialized plastics with enhanced thermal management and battery casing properties.

Growth Accelerators in the Automotive Plastics Industry

Long-term growth will be fueled by continuous technological advancements in materials science, resulting in lighter, stronger, and more sustainable plastics. Strategic partnerships between material suppliers and automotive manufacturers will accelerate innovation and adoption. Market expansion into emerging economies and the development of new applications for electric vehicles will drive further growth.

Key Players Shaping the Automotive Plastics Industry Market

- LANXESS

- Exxon Mobil Corporation

- Braskem

- Celanese Corporation

- BASF SE

- DSM

- DuPont

- Daicel Corporation

- Asahi Kasei Advance Corporation

- Covestro AG

- Borealis AG

Notable Milestones in Automotive Plastics Industry Sector

- September 2022: Citroën and BASF unveiled their all-electric concept car oli [all-ë], showcasing lightweighting and resource reduction through plastics.

- March 2022: Covestro AG expanded its polycarbonate compounding production capacity in India to meet growing demand.

In-Depth Automotive Plastics Industry Market Outlook

The automotive plastics market is poised for sustained growth over the forecast period, driven by technological innovations, increasing demand for EVs, and the rising focus on sustainability. Strategic partnerships, targeted investments in R&D, and expansion into new markets will be crucial for companies to capitalize on future opportunities and maintain competitiveness. The shift towards lighter, more durable, and environmentally friendly materials presents significant growth potential for innovative players.

Automotive Plastics Industry Segmentation

-

1. Material

- 1.1. Polypropylene (PP)

- 1.2. Polyurethane (PU)

- 1.3. Polyvinyl Chloride (PVC)

- 1.4. Polyethylene (PE)

- 1.5. Acrylonitrile Butadiene Styrene (ABS)

- 1.6. Polyamides (PA)

- 1.7. Polycarbonate (PC)

- 1.8. Other Materials

-

2. Application

- 2.1. Exterior

- 2.2. Interior

- 2.3. Under Bonnet

- 2.4. Other Applications

-

3. Vehicle Type

- 3.1. Conventional/Traditional Vehicles

- 3.2. Electric Vehicles

Automotive Plastics Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

- 2.4. Rest of North America

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Automotive Plastics Industry Regional Market Share

Geographic Coverage of Automotive Plastics Industry

Automotive Plastics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Polypropylene (PP)

- 5.1.2. Polyurethane (PU)

- 5.1.3. Polyvinyl Chloride (PVC)

- 5.1.4. Polyethylene (PE)

- 5.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 5.1.6. Polyamides (PA)

- 5.1.7. Polycarbonate (PC)

- 5.1.8. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Exterior

- 5.2.2. Interior

- 5.2.3. Under Bonnet

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Conventional/Traditional Vehicles

- 5.3.2. Electric Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Global Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Polypropylene (PP)

- 6.1.2. Polyurethane (PU)

- 6.1.3. Polyvinyl Chloride (PVC)

- 6.1.4. Polyethylene (PE)

- 6.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 6.1.6. Polyamides (PA)

- 6.1.7. Polycarbonate (PC)

- 6.1.8. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Exterior

- 6.2.2. Interior

- 6.2.3. Under Bonnet

- 6.2.4. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.3.1. Conventional/Traditional Vehicles

- 6.3.2. Electric Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Asia Pacific Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Polypropylene (PP)

- 7.1.2. Polyurethane (PU)

- 7.1.3. Polyvinyl Chloride (PVC)

- 7.1.4. Polyethylene (PE)

- 7.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 7.1.6. Polyamides (PA)

- 7.1.7. Polycarbonate (PC)

- 7.1.8. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Exterior

- 7.2.2. Interior

- 7.2.3. Under Bonnet

- 7.2.4. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.3.1. Conventional/Traditional Vehicles

- 7.3.2. Electric Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. North America Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Polypropylene (PP)

- 8.1.2. Polyurethane (PU)

- 8.1.3. Polyvinyl Chloride (PVC)

- 8.1.4. Polyethylene (PE)

- 8.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 8.1.6. Polyamides (PA)

- 8.1.7. Polycarbonate (PC)

- 8.1.8. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Exterior

- 8.2.2. Interior

- 8.2.3. Under Bonnet

- 8.2.4. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.3.1. Conventional/Traditional Vehicles

- 8.3.2. Electric Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Europe Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Polypropylene (PP)

- 9.1.2. Polyurethane (PU)

- 9.1.3. Polyvinyl Chloride (PVC)

- 9.1.4. Polyethylene (PE)

- 9.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 9.1.6. Polyamides (PA)

- 9.1.7. Polycarbonate (PC)

- 9.1.8. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Exterior

- 9.2.2. Interior

- 9.2.3. Under Bonnet

- 9.2.4. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.3.1. Conventional/Traditional Vehicles

- 9.3.2. Electric Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. South America Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Polypropylene (PP)

- 10.1.2. Polyurethane (PU)

- 10.1.3. Polyvinyl Chloride (PVC)

- 10.1.4. Polyethylene (PE)

- 10.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 10.1.6. Polyamides (PA)

- 10.1.7. Polycarbonate (PC)

- 10.1.8. Other Materials

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Exterior

- 10.2.2. Interior

- 10.2.3. Under Bonnet

- 10.2.4. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.3.1. Conventional/Traditional Vehicles

- 10.3.2. Electric Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Middle East and Africa Automotive Plastics Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Material

- 11.1.1. Polypropylene (PP)

- 11.1.2. Polyurethane (PU)

- 11.1.3. Polyvinyl Chloride (PVC)

- 11.1.4. Polyethylene (PE)

- 11.1.5. Acrylonitrile Butadiene Styrene (ABS)

- 11.1.6. Polyamides (PA)

- 11.1.7. Polycarbonate (PC)

- 11.1.8. Other Materials

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Exterior

- 11.2.2. Interior

- 11.2.3. Under Bonnet

- 11.2.4. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 11.3.1. Conventional/Traditional Vehicles

- 11.3.2. Electric Vehicles

- 11.1. Market Analysis, Insights and Forecast - by Material

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 LANXESS*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Exxon Mobil Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Braskem

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Celanese Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BASF SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 DSM

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 DuPont

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Daicel Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Asahi Kasei Advance Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Covestro AG

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Borealis AG

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 LANXESS*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Plastics Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Automotive Plastics Industry Revenue (billion), by Material 2025 & 2033

- Figure 3: Asia Pacific Automotive Plastics Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: Asia Pacific Automotive Plastics Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific Automotive Plastics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Automotive Plastics Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 7: Asia Pacific Automotive Plastics Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 8: Asia Pacific Automotive Plastics Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Asia Pacific Automotive Plastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Automotive Plastics Industry Revenue (billion), by Material 2025 & 2033

- Figure 11: North America Automotive Plastics Industry Revenue Share (%), by Material 2025 & 2033

- Figure 12: North America Automotive Plastics Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: North America Automotive Plastics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Automotive Plastics Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 15: North America Automotive Plastics Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 16: North America Automotive Plastics Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: North America Automotive Plastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Automotive Plastics Industry Revenue (billion), by Material 2025 & 2033

- Figure 19: Europe Automotive Plastics Industry Revenue Share (%), by Material 2025 & 2033

- Figure 20: Europe Automotive Plastics Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Europe Automotive Plastics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Europe Automotive Plastics Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 23: Europe Automotive Plastics Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 24: Europe Automotive Plastics Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Europe Automotive Plastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Automotive Plastics Industry Revenue (billion), by Material 2025 & 2033

- Figure 27: South America Automotive Plastics Industry Revenue Share (%), by Material 2025 & 2033

- Figure 28: South America Automotive Plastics Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: South America Automotive Plastics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: South America Automotive Plastics Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 31: South America Automotive Plastics Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 32: South America Automotive Plastics Industry Revenue (billion), by Country 2025 & 2033

- Figure 33: South America Automotive Plastics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Automotive Plastics Industry Revenue (billion), by Material 2025 & 2033

- Figure 35: Middle East and Africa Automotive Plastics Industry Revenue Share (%), by Material 2025 & 2033

- Figure 36: Middle East and Africa Automotive Plastics Industry Revenue (billion), by Application 2025 & 2033

- Figure 37: Middle East and Africa Automotive Plastics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East and Africa Automotive Plastics Industry Revenue (billion), by Vehicle Type 2025 & 2033

- Figure 39: Middle East and Africa Automotive Plastics Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 40: Middle East and Africa Automotive Plastics Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Automotive Plastics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 2: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 4: Global Automotive Plastics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 6: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 8: Global Automotive Plastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: China Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: India Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Japan Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: South Korea Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 15: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 17: Global Automotive Plastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: United States Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Canada Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Mexico Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of North America Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 23: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 25: Global Automotive Plastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Germany Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: France Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Italy Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 32: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 34: Global Automotive Plastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Brazil Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Argentina Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of South America Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Plastics Industry Revenue billion Forecast, by Material 2020 & 2033

- Table 39: Global Automotive Plastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 40: Global Automotive Plastics Industry Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 41: Global Automotive Plastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Saudi Arabia Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Africa Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of Middle East and Africa Automotive Plastics Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Plastics Industry?

The projected CAGR is approximately 5.01%.

2. Which companies are prominent players in the Automotive Plastics Industry?

Key companies in the market include LANXESS*List Not Exhaustive, Exxon Mobil Corporation, Braskem, Celanese Corporation, BASF SE, DSM, DuPont, Daicel Corporation, Asahi Kasei Advance Corporation, Covestro AG, Borealis AG.

3. What are the main segments of the Automotive Plastics Industry?

The market segments include Material, Application, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 598.24 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Lightweight Materials from Electric and Hybrid Vehicles; Other Drivers.

6. What are the notable trends driving market growth?

High Demand in Automotive Applications.

7. Are there any restraints impacting market growth?

Challenges Associated with Plastic Recycling; Other Restraints.

8. Can you provide examples of recent developments in the market?

September 2022: Citroën and BASF unveiled their all-electric concept car oli [all-ë], a manifesto to how much can be saved by reducing weight and resource usage. BASF has been pursuing an ambitious sustainability strategy for years now. Some of the major cornerstones of this strategy include the ChemCyclingTM project on improving the chemical recycling of plastics, as well as the biomass balance approach, in which fossil resources are replaced with renewables in production.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Plastics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Plastics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Plastics Industry?

To stay informed about further developments, trends, and reports in the Automotive Plastics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence