Key Insights

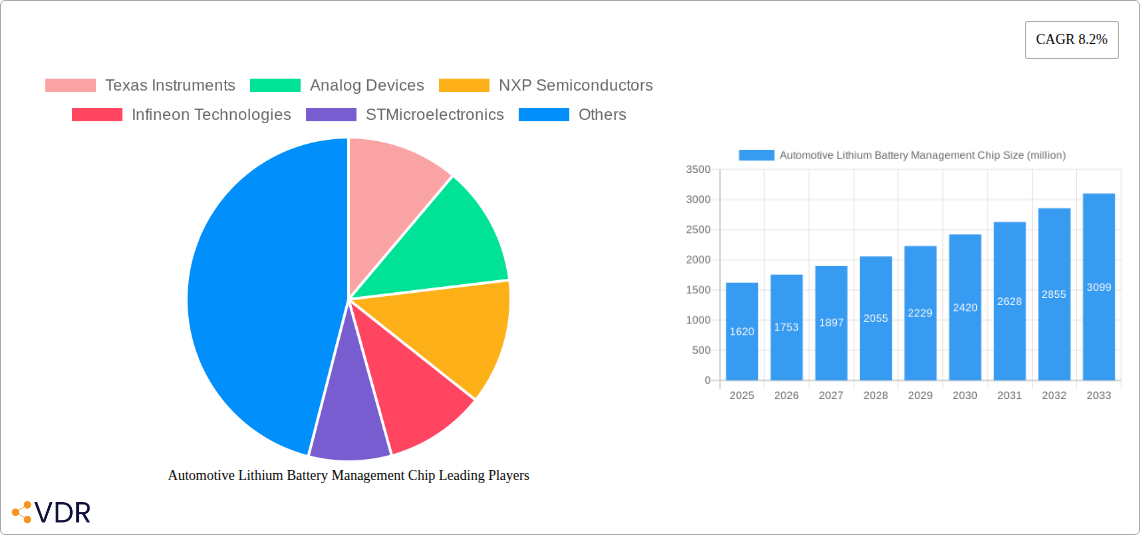

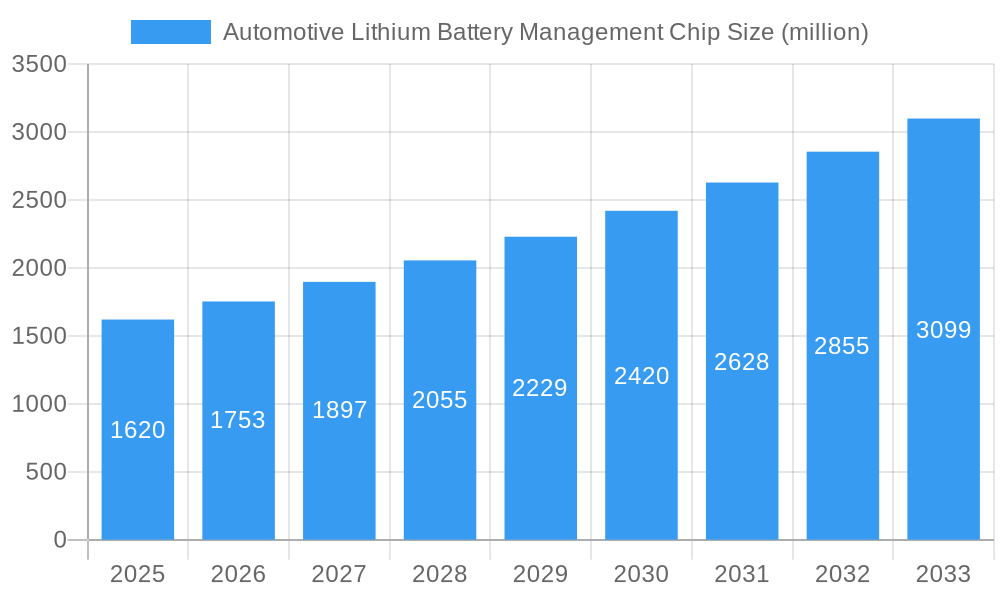

The global Automotive Lithium Battery Management Chip market is poised for substantial growth, projected to reach a valuation of $1620 million by 2025. This expansion is driven by a robust Compound Annual Growth Rate (CAGR) of 8.2% anticipated over the forecast period extending to 2033. The escalating demand for electric vehicles (EVs) and the increasing adoption of lithium-ion batteries across various automotive applications are the primary catalysts fueling this market surge. As governments worldwide implement stricter emission regulations and incentivize EV adoption, the need for sophisticated battery management systems (BMS) becomes paramount. These chips are crucial for optimizing battery performance, ensuring safety, extending battery lifespan, and enabling efficient charging, all of which are critical for the widespread acceptance and performance of EVs.

Automotive Lithium Battery Management Chip Market Size (In Billion)

The market is segmented by key applications, with Automotive Electronics taking the lead, followed by Energy and Electronics, and other niche applications. Within types, Battery Fuel Gauge ICs are expected to dominate due to their essential role in providing accurate State of Charge (SoC) and State of Health (SoH) information. Battery Charger ICs and Battery Authentication ICs also represent significant growth areas as the complexity and safety requirements of EV batteries continue to evolve. Key players such as Texas Instruments, Analog Devices, NXP Semiconductors, Infineon Technologies, and STMicroelectronics are actively investing in research and development to innovate and capture a larger market share. Emerging trends include the integration of advanced algorithms for predictive maintenance, enhanced thermal management, and bidirectional charging capabilities, further solidifying the indispensable role of these chips in the future of automotive power systems.

Automotive Lithium Battery Management Chip Company Market Share

Unveiling the Future: Automotive Lithium Battery Management Chip Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the global Automotive Lithium Battery Management Chip market, exploring its intricate dynamics, growth trajectory, and competitive landscape from 2019 to 2033. With the electric vehicle (EV) revolution accelerating, the demand for sophisticated battery management systems (BMS) is paramount. This report delves into the core technologies, market segmentation, regional dominance, and key players driving innovation in this critical sector. We analyze the parent market of automotive semiconductors and the child market of specialized battery management ICs, offering a holistic view of the value chain and its future potential.

Automotive Lithium Battery Management Chip Market Dynamics & Structure

The Automotive Lithium Battery Management Chip market is characterized by a moderate to high concentration, with leading semiconductor manufacturers actively investing in research and development to cater to the escalating demands of the automotive industry. Technological innovation remains the primary driver, fueled by the pursuit of higher energy density, faster charging capabilities, enhanced safety features, and extended battery lifespan for electric vehicles. Regulatory frameworks, such as stringent safety standards and emissions targets, are also playing a pivotal role in shaping market trends and pushing for advanced BMS solutions. Competitive product substitutes, while present in basic battery monitoring, are increasingly unable to meet the complex requirements of modern lithium-ion battery packs in automotive applications. End-user demographics are shifting towards early adopters of EVs and consumers prioritizing sustainability and lower running costs. Mergers and acquisitions (M&A) are a significant trend, with larger players acquiring specialized technology firms to bolster their portfolios and gain a competitive edge.

- Market Concentration: Moderate to High, with key players holding substantial market share.

- Technological Innovation Drivers: Increased EV adoption, demand for longer range, faster charging, enhanced safety, and improved battery longevity.

- Regulatory Frameworks: Stringent safety standards (e.g., ISO 26262), emissions regulations, and government incentives for EVs.

- Competitive Product Substitutes: Limited for high-performance automotive BMS; basic solutions exist for non-automotive applications.

- End-User Demographics: Growing segment of environmentally conscious consumers, tech-savvy early adopters, and fleet operators seeking operational efficiency.

- M&A Trends: Strategic acquisitions to gain access to advanced technologies, talent, and market share. Approximately 15-20 significant M&A deals are projected in the forecast period.

Automotive Lithium Battery Management Chip Growth Trends & Insights

The Automotive Lithium Battery Management Chip market is poised for exceptional growth, projected to reach significant market size by 2033. This expansion is driven by the exponential rise in electric vehicle production globally, coupled with increasingly stringent performance and safety requirements for battery packs. Adoption rates for advanced BMS solutions are directly correlated with EV penetration, which is expected to see a compound annual growth rate (CAGR) of approximately 25-30% over the forecast period. Technological disruptions, including advancements in AI for predictive maintenance and sophisticated algorithms for cell balancing, are creating new avenues for market growth. Consumer behavior is also shifting, with a growing emphasis on vehicle range, charging infrastructure availability, and the overall cost of ownership, all of which are directly influenced by effective battery management. The market penetration of sophisticated BMS solutions within new EV models is expected to rise from around 70% in the base year to over 90% by 2033. The increasing complexity of battery chemistries and higher voltage architectures further necessitates the adoption of intelligent and robust battery management chips.

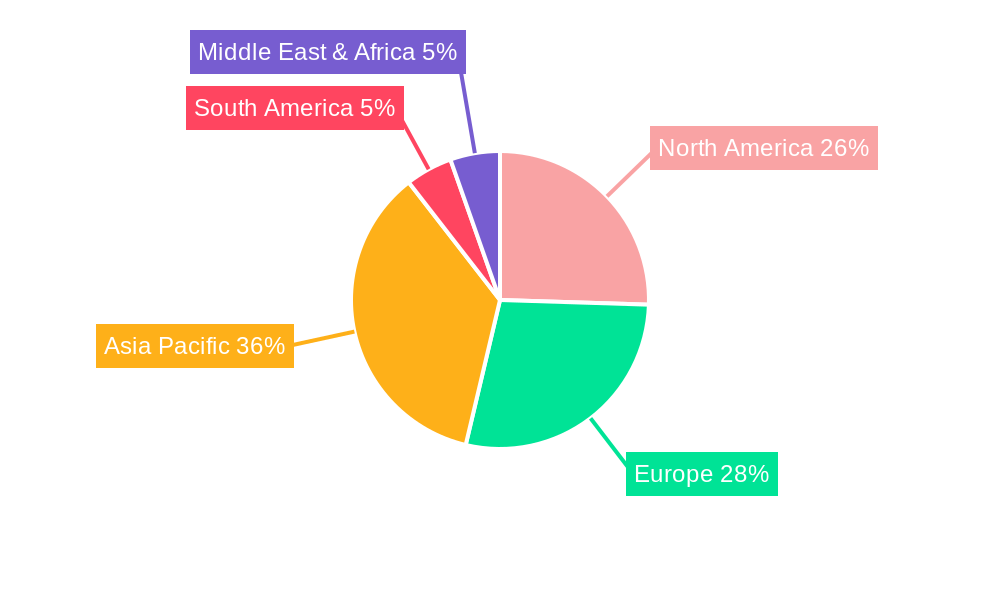

Dominant Regions, Countries, or Segments in Automotive Lithium Battery Management Chip

The Automotive Electronics segment, specifically within the Application category, is the undisputed leader in the Automotive Lithium Battery Management Chip market. This dominance is fueled by the relentless surge in electric vehicle production and the critical need for advanced BMS to ensure safety, performance, and longevity of EV batteries. Within this segment, Battery Charger ICs and Battery Fuel Gauge ICs are the most significant types, forming the backbone of any functional battery management system. Geographically, Asia Pacific, particularly China, is the largest and fastest-growing market, owing to its position as the global hub for EV manufacturing and strong government support for the new energy vehicle industry. The region benefits from extensive investments in battery technology and a robust supply chain for electronic components. North America and Europe follow closely, driven by increasing EV adoption, supportive policies, and the presence of major automotive manufacturers with aggressive electrification strategies.

- Dominant Application Segment: Automotive Electronics, accounting for an estimated 85% market share.

- Key Drivers: Surging EV production, increasing demand for battery safety and performance, stringent automotive regulations.

- Dominant Types: Battery Fuel Gauge ICs and Battery Charger ICs, collectively holding an estimated 70% share of the BMS IC market.

- Key Drivers: Essential for monitoring battery state-of-charge, state-of-health, charge control, and thermal management.

- Dominant Region: Asia Pacific, with China leading market growth and production.

- Key Drivers: Massive EV manufacturing capacity, supportive government policies, extensive battery supply chain, growing consumer demand.

- Leading Country: China, projected to contribute over 40% of the global market revenue by 2033.

- Key Drivers: Dominant EV market share, advanced battery technology development, integrated supply chain.

- Growth Potential: Significant growth opportunities exist in emerging markets with increasing EV adoption and supportive policies.

Automotive Lithium Battery Management Chip Product Landscape

The product landscape for Automotive Lithium Battery Management Chips is marked by continuous innovation, focusing on miniaturization, enhanced accuracy, and superior thermal management capabilities. Key product types include Battery Fuel Gauge ICs, crucial for precise state-of-charge (SoC) and state-of-health (SoH) estimation, and Battery Charger ICs, designed for efficient and safe charging protocols. Battery Authentication ICs are gaining prominence for their role in enhancing battery security and preventing counterfeiting. Manufacturers are differentiating their offerings through integrated solutions that combine multiple BMS functions onto a single chip, thereby reducing system complexity and cost. Advanced features such as multi-cell balancing, over-voltage/under-voltage protection, and integrated safety mechanisms are becoming standard. The trend towards higher energy density batteries necessitates chips capable of managing higher voltages and currents with exceptional precision and reliability.

Key Drivers, Barriers & Challenges in Automotive Lithium Battery Management Chip

The Automotive Lithium Battery Management Chip market is propelled by several key drivers, primarily the accelerating adoption of electric vehicles worldwide and the growing demand for enhanced battery safety, performance, and longevity. Technological advancements in lithium-ion battery chemistry, leading to higher energy densities, also necessitate more sophisticated management solutions. Government regulations and incentives aimed at promoting EV adoption and reducing carbon emissions further act as significant catalysts.

However, the market faces certain barriers and challenges. The high cost of advanced BMS components can be a restraint, especially for entry-level EV models. Supply chain disruptions, particularly concerning critical raw materials and semiconductor manufacturing capacity, pose a significant challenge. The increasing complexity of battery systems and the need for stringent safety certifications (e.g., ISO 26262 compliance) require substantial R&D investment and long development cycles. Furthermore, intense competition among established players and emerging entrants can put pressure on profit margins.

- Key Drivers:

- Exponential growth in EV production.

- Demand for improved battery safety, performance, and lifespan.

- Supportive government policies and regulations for EVs.

- Advancements in battery technology (e.g., higher energy density).

- Key Barriers & Challenges:

- High cost of advanced BMS solutions.

- Supply chain volatility and component shortages.

- Stringent safety regulations and long development cycles.

- Intense competition and pricing pressures.

- Need for continuous innovation to keep pace with battery technology.

Emerging Opportunities in Automotive Lithium Battery Management Chip

Emerging opportunities in the Automotive Lithium Battery Management Chip sector are largely driven by the evolving needs of the EV ecosystem. The development of solid-state batteries presents a new frontier, requiring entirely novel BMS architectures and chip designs. Opportunities also lie in the growing demand for Vehicle-to-Grid (V2G) and Vehicle-to-Everything (V2X) technologies, which necessitate more intelligent and bidirectional power management capabilities. The aftermarket for battery diagnostics and remanufacturing also presents a lucrative avenue for specialized BMS solutions. Furthermore, the integration of advanced AI and machine learning algorithms for predictive battery health monitoring and optimization offers significant potential for differentiation and value creation.

Growth Accelerators in the Automotive Lithium Battery Management Chip Industry

Several factors are acting as growth accelerators for the Automotive Lithium Battery Management Chip industry. Continuous technological breakthroughs in power semiconductor technology enable the development of smaller, more efficient, and cost-effective BMS chips. Strategic partnerships between semiconductor manufacturers, automotive OEMs, and battery producers are crucial for co-developing tailored solutions and streamlining integration. Market expansion into emerging economies with rapidly growing EV markets, coupled with favorable government policies, will further fuel demand. The increasing focus on battery recycling and second-life applications also opens up new opportunities for specialized management chips.

Key Players Shaping the Automotive Lithium Battery Management Chip Market

- Texas Instruments

- Analog Devices

- NXP Semiconductors

- Infineon Technologies

- STMicroelectronics

- Maxim (ADI)

- Onsemi

- Microchip

- Sensata

- Ablic

- Diodes Incorporated

- Sinowealth

- GigaDevice Semiconductor

- Southchip Semiconductor Technology

Notable Milestones in Automotive Lithium Battery Management Chip Sector

- 2019-2020: Increased adoption of highly integrated BMS solutions with multi-cell monitoring capabilities.

- 2021: Advancements in Battery Fuel Gauge ICs offering higher accuracy and improved temperature compensation.

- 2022: Introduction of Battery Authentication ICs to enhance battery security and prevent counterfeiting.

- 2023: Growing focus on AI-driven predictive battery health monitoring algorithms integrated into BMS chips.

- 2024: Development of highly efficient Battery Charger ICs supporting ultra-fast charging technologies.

- 2025 (Estimated): Emergence of BMS solutions for next-generation battery chemistries like solid-state batteries.

- 2026-2033 (Forecast): Significant advancements in bidirectional charging capabilities for V2G and V2X applications.

In-Depth Automotive Lithium Battery Management Chip Market Outlook

The Automotive Lithium Battery Management Chip market is set for sustained and robust growth, driven by the irreversible shift towards electric mobility. Future market potential lies in the continuous miniaturization and integration of BMS functionalities, leading to cost reductions and improved vehicle packaging. Strategic opportunities will emerge from the development of specialized chips for advanced battery chemistries, such as solid-state and silicon-anode batteries, and for emerging applications like autonomous driving systems that demand higher power efficiency. The industry's ability to navigate supply chain complexities and adapt to evolving regulatory landscapes will be critical for realizing this expansive future.

Automotive Lithium Battery Management Chip Segmentation

-

1. Application

- 1.1. Automotive Electronics

- 1.2. Energy and Electronics

- 1.3. Others

-

2. Types

- 2.1. Battery Fuel Gauge IC

- 2.2. Battery Charger IC

- 2.3. Battery Authentication IC

Automotive Lithium Battery Management Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Lithium Battery Management Chip Regional Market Share

Geographic Coverage of Automotive Lithium Battery Management Chip

Automotive Lithium Battery Management Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive Electronics

- 5.1.2. Energy and Electronics

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Battery Fuel Gauge IC

- 5.2.2. Battery Charger IC

- 5.2.3. Battery Authentication IC

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive Electronics

- 6.1.2. Energy and Electronics

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Battery Fuel Gauge IC

- 6.2.2. Battery Charger IC

- 6.2.3. Battery Authentication IC

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive Electronics

- 7.1.2. Energy and Electronics

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Battery Fuel Gauge IC

- 7.2.2. Battery Charger IC

- 7.2.3. Battery Authentication IC

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive Electronics

- 8.1.2. Energy and Electronics

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Battery Fuel Gauge IC

- 8.2.2. Battery Charger IC

- 8.2.3. Battery Authentication IC

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive Electronics

- 9.1.2. Energy and Electronics

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Battery Fuel Gauge IC

- 9.2.2. Battery Charger IC

- 9.2.3. Battery Authentication IC

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Lithium Battery Management Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive Electronics

- 10.1.2. Energy and Electronics

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Battery Fuel Gauge IC

- 10.2.2. Battery Charger IC

- 10.2.3. Battery Authentication IC

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Texas Instruments

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Analog Devices

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 NXP Semiconductors

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Infineon Technologies

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 STMicroelectronics

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Switching Chargers

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Battery Protection Ics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Maxim (ADI)

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Onsemi

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Microchip

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sensata

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ablic

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Diodes Incorporated

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Sinowealth

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 GigaDevice Semiconductor

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Southchip Semiconductor Technology

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Texas Instruments

List of Figures

- Figure 1: Global Automotive Lithium Battery Management Chip Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Lithium Battery Management Chip Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Lithium Battery Management Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Lithium Battery Management Chip Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Lithium Battery Management Chip Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Lithium Battery Management Chip Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Lithium Battery Management Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Lithium Battery Management Chip Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Lithium Battery Management Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Lithium Battery Management Chip Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Lithium Battery Management Chip Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Lithium Battery Management Chip Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Lithium Battery Management Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Lithium Battery Management Chip Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Lithium Battery Management Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Lithium Battery Management Chip Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Lithium Battery Management Chip Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Lithium Battery Management Chip Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Lithium Battery Management Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Lithium Battery Management Chip Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Lithium Battery Management Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Lithium Battery Management Chip Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Lithium Battery Management Chip Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Lithium Battery Management Chip Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Lithium Battery Management Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Lithium Battery Management Chip Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Lithium Battery Management Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Lithium Battery Management Chip Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Lithium Battery Management Chip Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Lithium Battery Management Chip Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Lithium Battery Management Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Lithium Battery Management Chip Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Lithium Battery Management Chip Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Lithium Battery Management Chip?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the Automotive Lithium Battery Management Chip?

Key companies in the market include Texas Instruments, Analog Devices, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Switching Chargers, Battery Protection Ics, Maxim (ADI), Onsemi, Microchip, Sensata, Ablic, Diodes Incorporated, Sinowealth, GigaDevice Semiconductor, Southchip Semiconductor Technology.

3. What are the main segments of the Automotive Lithium Battery Management Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1620 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Lithium Battery Management Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Lithium Battery Management Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Lithium Battery Management Chip?

To stay informed about further developments, trends, and reports in the Automotive Lithium Battery Management Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence