Key Insights

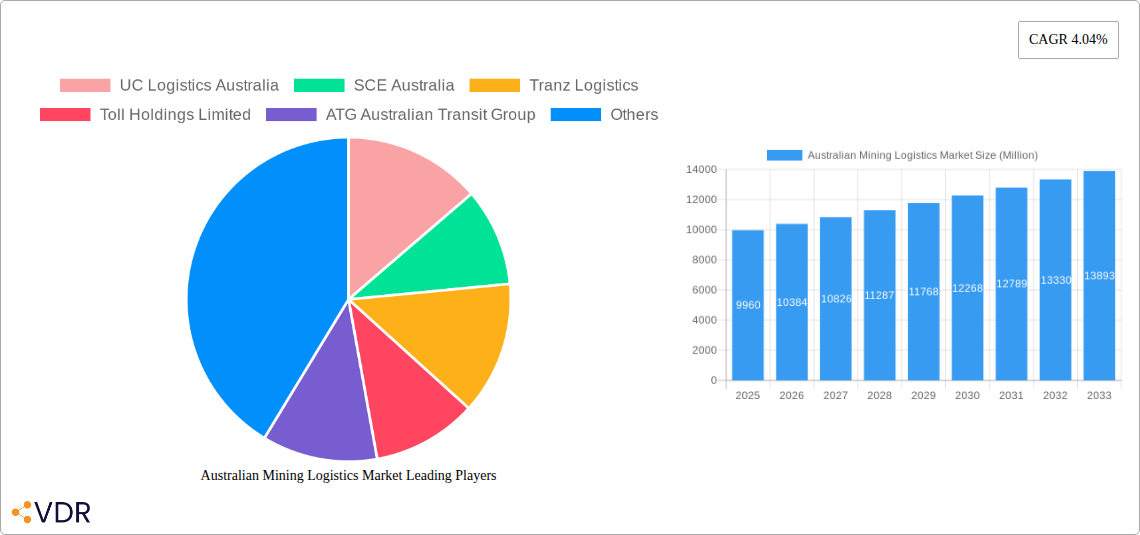

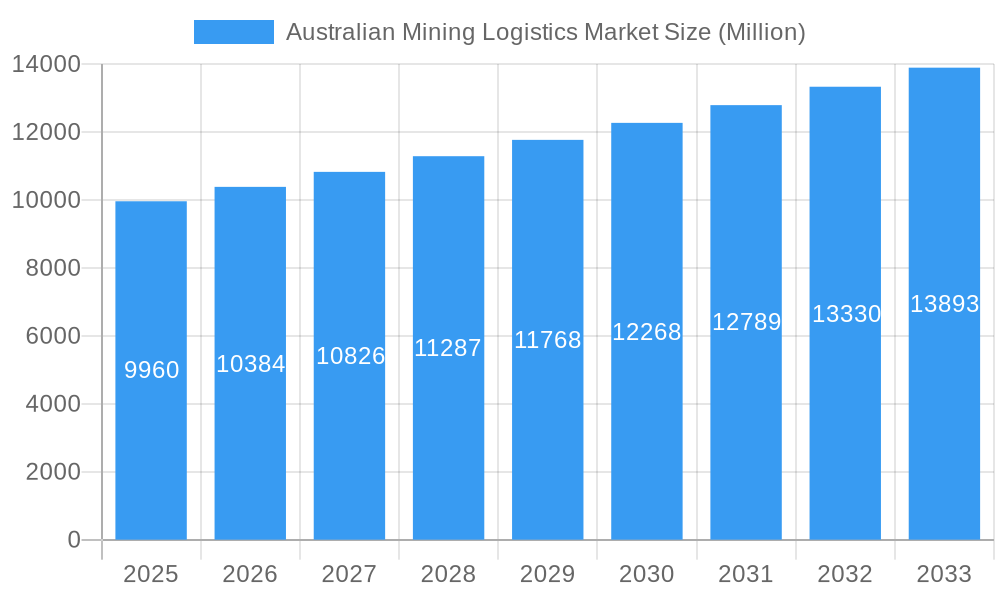

The Australian mining logistics market, valued at $9.96 billion in 2025, is poised for steady growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 4.04% from 2025 to 2033. This growth is fueled by several key factors. Increased mining activities, driven by rising global demand for resources like iron ore, base metals, and coal, are creating significant demand for efficient transportation and warehousing solutions. Furthermore, the industry's ongoing adoption of advanced technologies, such as GPS tracking, optimized routing software, and improved inventory management systems, enhances operational efficiency and reduces costs. The rise of value-added services, such as specialized handling for sensitive materials and customized logistics solutions tailored to individual mining operations, further contributes to market expansion. Key players like Linfox Pty Ltd, Toll Holdings Limited, and others are actively investing in infrastructure and technological upgrades to meet the growing demands. Competition is intensifying, with companies focusing on strategic partnerships and acquisitions to gain market share and expand their service offerings. However, challenges such as fluctuating commodity prices, infrastructure limitations in remote mining regions, and stringent environmental regulations could potentially restrain market growth to some degree.

Australian Mining Logistics Market Market Size (In Billion)

The segmentation of the market reveals significant opportunities within various service categories. Transportation services, encompassing rail, road, and maritime freight, constitute a substantial portion of the market. Warehousing and inventory management, crucial for efficient resource handling and supply chain optimization, are also key segments experiencing growth. The strong demand for iron ore, base metals, and coal drives a considerable portion of the overall logistics needs, with the “Others” category encompassing specialized minerals and metals expected to witness increasing demand in the coming years. Regional variations within Australia exist, with higher concentration of logistics activities near major mining hubs. The forecast period (2025-2033) anticipates sustained growth, driven by consistent mining output and investment in infrastructural improvements to support the industry’s expansion. The market's future hinges on the interplay of global commodity prices, technological advancements, and government regulations aimed at promoting sustainable mining practices.

Australian Mining Logistics Market Company Market Share

Australian Mining Logistics Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Australian mining logistics market, encompassing market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. The report segments the market by service (Transportation, Warehousing and Inventory Management, Value-added Services) and mineral/metal type (Iron Ore, Base Metals, Coal, Gold, Others), offering granular insights into this crucial sector. The total market size is projected at xx Million in 2025.

Australian Mining Logistics Market Dynamics & Structure

The Australian mining logistics market is characterized by a moderate level of concentration, with several large players dominating specific segments. Market share is distributed amongst major players, including Linfox Pty Ltd, Toll Holdings Limited, and ATG Australian Transit Group, each holding a significant percentage. However, smaller specialized companies also play a vital role. Technological innovation, driven by automation, data analytics, and digitalization, is a key driver, though implementation faces challenges due to high upfront investment and integration complexities. The regulatory framework, encompassing safety and environmental regulations, significantly influences operational costs and strategies. Substitute services are limited, strengthening the market's resilience. The market exhibits significant end-user diversity, catering to various mining operations across different commodities. Recent years have witnessed a moderate level of M&A activity, largely focused on consolidating transportation and warehousing services, with an estimated xx M&A deals in the past five years.

- Market Concentration: Moderately concentrated, with key players holding significant shares.

- Technological Innovation: Automation, data analytics, and digitalization are major drivers, but high upfront costs are a barrier.

- Regulatory Framework: Stringent safety and environmental regulations influence costs and operations.

- Competitive Substitutes: Limited substitutes bolster market stability.

- M&A Activity: Moderate activity focused on service consolidation. Estimated xx deals (2019-2024).

Australian Mining Logistics Market Growth Trends & Insights

The Australian mining logistics market is experiencing robust growth, fueled by rising mining activity, especially in the iron ore and coal sectors. The market witnessed a CAGR of xx% during the historical period (2019-2024) and is projected to maintain a healthy CAGR of xx% during the forecast period (2025-2033). This growth is driven by increasing production volumes, expanding mining operations, and growing demand for efficient logistics solutions. Technological disruptions, such as the adoption of autonomous vehicles and improved tracking systems, are further accelerating market expansion. Shifting consumer behavior, emphasizing sustainability and efficiency, influences logistical choices. Market penetration of advanced technologies remains relatively low but is expected to increase steadily.

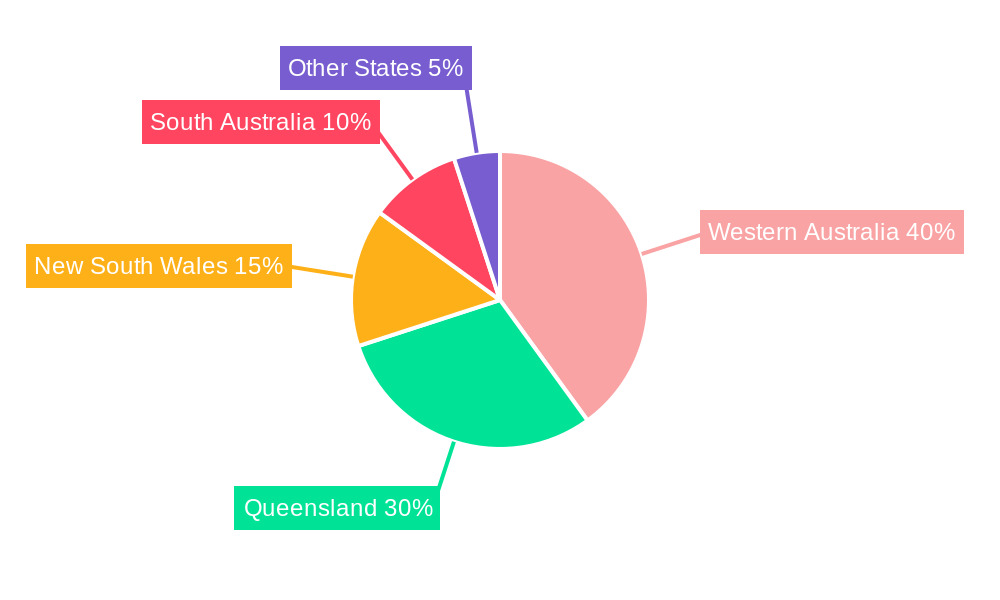

Dominant Regions, Countries, or Segments in Australian Mining Logistics Market

Western Australia and Queensland, major mining hubs, dominate the Australian mining logistics market. Their dominance stems from a high concentration of mining operations, extensive infrastructure, and supportive government policies. The transportation segment, particularly road haulage, commands the largest market share due to the prevalence of shorter-haul transportation needs. Iron ore and coal account for the largest share of transported minerals due to their high production volumes. However, the increasing focus on lithium and other battery minerals is presenting lucrative growth opportunities for specialized logistics providers.

- Key Drivers: High mining activity, supportive infrastructure, government policies, and growing demand for specialized logistics services.

- Western Australia & Queensland: Dominant regions due to concentrated mining activities and infrastructure.

- Transportation Segment: Largest share, driven by prevalent road haulage demands.

- Iron Ore & Coal: Major contributors due to high production volumes.

Australian Mining Logistics Market Product Landscape

The market offers a range of services, including transportation (road, rail, and maritime), warehousing and inventory management, and value-added services like specialized handling and packaging for sensitive minerals. Recent innovations include real-time tracking systems, predictive maintenance for vehicles, and automated warehousing solutions enhancing efficiency and transparency. These advancements are characterized by increased automation, improved data analytics, and a focus on safety and environmental responsibility. Unique selling propositions focus on speed, reliability, security, and customized solutions tailored to the specific needs of different mining operations.

Key Drivers, Barriers & Challenges in Australian Mining Logistics Market

Key Drivers:

- Growing mining production across various minerals.

- Increasing demand for efficient and cost-effective logistics solutions.

- Technological advancements improving efficiency and transparency.

- Government initiatives promoting infrastructure development.

Challenges:

- Infrastructure constraints (road congestion, rail capacity) impacting delivery times and costs. These constraints lead to approximately xx Million in annual revenue loss.

- Fluctuations in commodity prices impacting demand and investment decisions.

- Skilled labor shortages impacting operational efficiency.

- Stringent environmental regulations increasing operational costs.

Emerging Opportunities in Australian Mining Logistics Market

- Growing demand for lithium and other battery minerals creating specialized logistics needs.

- Increasing focus on sustainable and environmentally friendly logistics solutions.

- Adoption of autonomous vehicles and drones improving efficiency and safety.

- Expansion of digitalization and data analytics providing real-time visibility and optimization.

Growth Accelerators in the Australian Mining Logistics Market Industry

Technological advancements such as the Internet of Things (IoT) and Artificial Intelligence (AI) are key catalysts, enabling real-time tracking, predictive maintenance, and route optimization. Strategic partnerships between logistics providers and mining companies are streamlining operations. Government investments in infrastructure upgrades, including road and rail networks, are crucial in supporting growth.

Key Players Shaping the Australian Mining Logistics Market Market

- UC Logistics Australia

- SCE Australia

- Tranz Logistics

- Toll Holdings Limited

- ATG Australian Transit Group

- Centurion

- Campbell Transport

- National Group

- Linfox Pty Ltd

- Vale

- Kalari

- Bis Industries

Notable Milestones in Australian Mining Logistics Market Sector

- March 2022: Rio Tinto's USD 825 million acquisition of the Rincon lithium project signals increased activity in the lithium logistics sector.

- January 2022: Bis Industries' multi-year haulage contract with Hunter Valley Operations highlights ongoing demand for specialized transportation services.

In-Depth Australian Mining Logistics Market Market Outlook

The Australian mining logistics market is poised for continued strong growth, driven by sustained mining activity, technological advancements, and strategic investments. The market's future potential is considerable, particularly in specialized sectors like lithium logistics and the adoption of sustainable practices. Opportunities exist for companies offering innovative solutions, such as autonomous vehicles and digital platforms, to capture market share and drive long-term value.

Australian Mining Logistics Market Segmentation

-

1. Service

- 1.1. Transportation

- 1.2. Warehousing and Inventory Management

- 1.3. Value-added Services

-

2. Mineral/Metal

- 2.1. Iron Ore

- 2.2. Base Metals

- 2.3. Coal

- 2.4. Gold

- 2.5. Others

Australian Mining Logistics Market Segmentation By Geography

- 1. Australia

Australian Mining Logistics Market Regional Market Share

Geographic Coverage of Australian Mining Logistics Market

Australian Mining Logistics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service

- 5.1.1. Transportation

- 5.1.2. Warehousing and Inventory Management

- 5.1.3. Value-added Services

- 5.2. Market Analysis, Insights and Forecast - by Mineral/Metal

- 5.2.1. Iron Ore

- 5.2.2. Base Metals

- 5.2.3. Coal

- 5.2.4. Gold

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Service

- 6. Australian Mining Logistics Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service

- 6.1.1. Transportation

- 6.1.2. Warehousing and Inventory Management

- 6.1.3. Value-added Services

- 6.2. Market Analysis, Insights and Forecast - by Mineral/Metal

- 6.2.1. Iron Ore

- 6.2.2. Base Metals

- 6.2.3. Coal

- 6.2.4. Gold

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Service

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 UC Logistics Australia

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 SCE Australia

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Tranz Logistics

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Toll Holdings Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ATG Australian Transit Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Centurion

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Campbell Transport**List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 National Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Linfox Pty Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Vale

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Kalari

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Bis Industries

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 UC Logistics Australia

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australian Mining Logistics Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australian Mining Logistics Market Share (%) by Company 2025

List of Tables

- Table 1: Australian Mining Logistics Market Revenue Million Forecast, by Service 2020 & 2033

- Table 2: Australian Mining Logistics Market Revenue Million Forecast, by Mineral/Metal 2020 & 2033

- Table 3: Australian Mining Logistics Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Australian Mining Logistics Market Revenue Million Forecast, by Service 2020 & 2033

- Table 5: Australian Mining Logistics Market Revenue Million Forecast, by Mineral/Metal 2020 & 2033

- Table 6: Australian Mining Logistics Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australian Mining Logistics Market?

The projected CAGR is approximately 4.04%.

2. Which companies are prominent players in the Australian Mining Logistics Market?

Key companies in the market include UC Logistics Australia, SCE Australia, Tranz Logistics, Toll Holdings Limited, ATG Australian Transit Group, Centurion, Campbell Transport**List Not Exhaustive, National Group, Linfox Pty Ltd, Vale, Kalari, Bis Industries.

3. What are the main segments of the Australian Mining Logistics Market?

The market segments include Service, Mineral/Metal.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.96 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Consumption of Frozen Food Driving the Market.

6. What are the notable trends driving market growth?

Increasing Exports from the Mining Industry.

7. Are there any restraints impacting market growth?

4.; Constantly Increasing Fuel Costs.

8. Can you provide examples of recent developments in the market?

March 2022: After approval from Australia's Foreign Investment Review Board, Rio Tinto has completed the USD 825 million acquisition of the Rincon lithium project in Argentina. In a time of limited supply, Rincon positioned Rio Tinto to meet the double-digit growth in lithium demand over the next ten years by strengthening their battery materials business. As they construct this project to the highest ESG standards, they will collaborate with neighborhood residents, the Province of Salta, and the Government of Argentina.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australian Mining Logistics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australian Mining Logistics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australian Mining Logistics Market?

To stay informed about further developments, trends, and reports in the Australian Mining Logistics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence