Key Insights

The Australian In Vitro Diagnostics (IVD) market is set for significant expansion, propelled by increased healthcare investment, a rising incidence of chronic and infectious diseases, and advancements in diagnostic technologies. The market is projected to reach a size of $1.96 billion by 2025, growing at a Compound Annual Growth Rate (CAGR) of 5.36% from 2025 to 2033. Key growth drivers include the escalating prevalence of conditions such as diabetes, cancer, and cardiovascular diseases, demanding sophisticated diagnostic solutions for early detection and effective management. The increasing adoption of molecular diagnostics and immunoassays, alongside supportive government initiatives aimed at enhancing healthcare infrastructure and access to advanced diagnostics, are also contributing factors. Demand for automated and point-of-care testing solutions is rising, offering healthcare professionals faster, more accurate diagnostic capabilities to improve patient outcomes and alleviate healthcare system pressures.

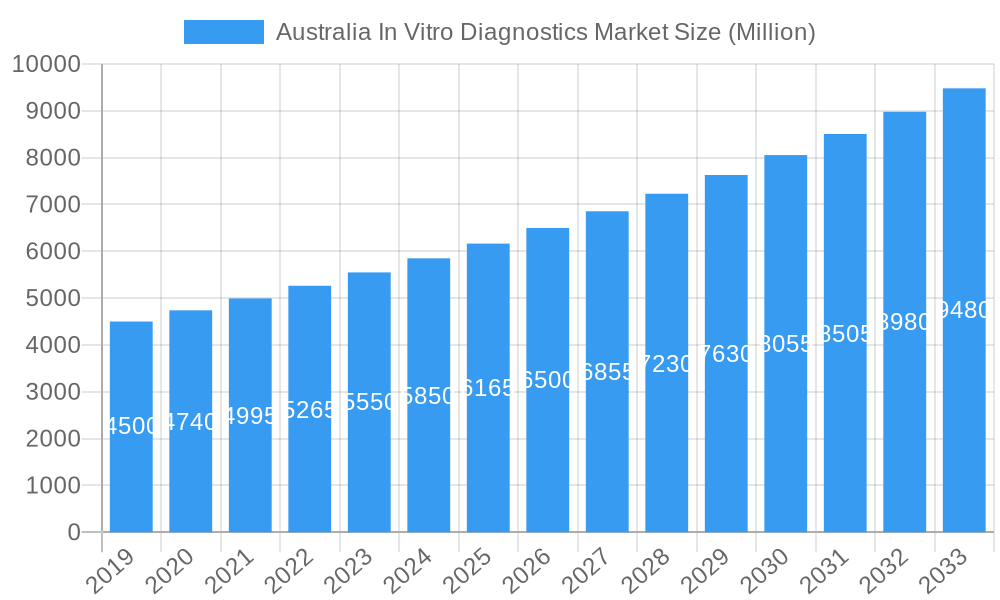

Australia In Vitro Diagnostics Market Market Size (In Billion)

Market segmentation reveals the diverse applications of IVD in Australia. Clinical Chemistry remains a dominant segment due to its routine use in health screenings and disease monitoring. However, Molecular Diagnostics is experiencing rapid growth, driven by the need for precise identification of genetic markers, infectious agents, and personalized medicine strategies, particularly in oncology and infectious disease management. Immuno Diagnostics also holds a critical position, with advancements in antibody-based assays enabling the detection of a wide array of biomarkers. Instruments and reagents constitute the primary product categories, with consistent demand for high-throughput, automated systems in laboratories and hospitals. Application segments such as Infectious Disease, Cancer/Oncology, and Diabetes are anticipated to show the highest growth, aligning with global health trends and Australia's specific disease burden. Leading market participants, including Abbott, Thermo Fisher Scientific, and F. Hoffmann-La Roche Ltd, are actively investing in research and development and forging strategic partnerships to meet evolving market demands and strengthen their presence in the Australian IVD sector.

Australia In Vitro Diagnostics Market Company Market Share

This report offers a comprehensive analysis of the Australian In Vitro Diagnostics (IVD) market, covering its current state, historical trajectory, and future outlook. We explore key market dynamics, technological innovations, regulatory landscapes, and competitive strategies influencing the industry. The analysis examines dominant segments, product advancements, and the critical drivers, challenges, and emerging opportunities within this crucial sector. With a study period from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this research provides strategic insights for stakeholders aiming to leverage the dynamic Australian IVD market. All market values are presented in billions of USD.

Australia In Vitro Diagnostics Market Market Dynamics & Structure

The Australian In Vitro Diagnostics (IVD) market is characterized by a moderately concentrated structure, with key global players like Abbott, Thermo Fisher Scientific, F Hoffmann-La Roche Ltd, and Siemens AG holding significant market shares. Technological innovation serves as a primary driver, fueled by advancements in molecular diagnostics, automation, and artificial intelligence, enabling faster, more accurate, and personalized diagnostic solutions. Regulatory frameworks, primarily governed by the Therapeutic Goods Administration (TGA), ensure product safety and efficacy, influencing market entry and product development. Competitive product substitutes are increasingly prevalent, particularly in areas like point-of-care testing, challenging traditional laboratory-based diagnostics. End-user demographics are shifting, with an increasing demand for home-based testing solutions and a growing preference for integrated diagnostic platforms. Mergers and acquisitions (M&A) trends are moderate, driven by the pursuit of expanded product portfolios, enhanced market reach, and technological integration. For instance, recent collaborations, like that between CerTest Biotec and BD for monkeypox diagnostics, highlight the strategic partnerships aimed at addressing emerging health concerns. Innovation barriers include the high cost of research and development, stringent regulatory approval processes, and the need for continuous investment in advanced infrastructure. The market is valued at approximately $1,800 million in 2025, with a projected CAGR of 6.5% during the forecast period.

- Market Concentration: Moderate, dominated by multinational corporations.

- Technological Innovation: Driven by molecular diagnostics, AI, and automation.

- Regulatory Frameworks: Governed by the TGA, ensuring product compliance.

- Competitive Substitutes: Growing in point-of-care and home testing segments.

- End-User Demographics: Shifting towards personalized and accessible diagnostics.

- M&A Trends: Moderate, focused on portfolio expansion and technological synergy.

- Innovation Barriers: High R&D costs, regulatory hurdles, infrastructure investment.

Australia In Vitro Diagnostics Market Growth Trends & Insights

The Australian In Vitro Diagnostics (IVD) market is poised for robust expansion, driven by a confluence of factors including an aging population, increasing prevalence of chronic diseases, and heightened awareness regarding early disease detection. The adoption rates for advanced diagnostic technologies are steadily rising, particularly in molecular diagnostics and immunoassay segments, as healthcare providers and patients recognize their superior accuracy and speed. Technological disruptions, such as the integration of artificial intelligence and machine learning in diagnostic algorithms, are transforming data analysis and interpretation, leading to more precise diagnoses and personalized treatment plans. Consumer behavior shifts are also playing a significant role, with a growing demand for convenient, accessible, and user-friendly diagnostic solutions, including home-based testing kits and point-of-care (POC) devices. The market size for IVD in Australia was approximately $1,500 million in 2023 and is projected to reach $3,200 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period (2025-2033). Market penetration of advanced diagnostics, which was around 30% in 2019, is expected to exceed 55% by 2033. The increasing incidence of infectious diseases, coupled with the ongoing need for rapid diagnostic tests, particularly following global health events like the COVID-19 pandemic, has accelerated the demand for a wide array of IVD products. Furthermore, advancements in liquid biopsy techniques are revolutionizing cancer diagnostics and monitoring, opening up new avenues for growth. The focus on preventative healthcare and early intervention strategies by the Australian government and healthcare institutions further fuels the demand for sophisticated diagnostic tools. The integration of digital health platforms and telemedicine is also creating opportunities for remote diagnostics and improved patient outcomes, thereby contributing to the sustained growth of the IVD market.

Dominant Regions, Countries, or Segments in Australia In Vitro Diagnostics Market

The Australian In Vitro Diagnostics (IVD) market's growth is primarily propelled by the Molecular Diagnostics segment within the Test Type category, and Diagnostic Laboratories as the leading End User. Reagents hold a dominant position in the Type of Product segment, while Infectious Disease applications are the key growth driver.

Molecular Diagnostics: This segment is experiencing exponential growth due to its precision in identifying genetic material of pathogens, crucial for rapid and accurate diagnosis of infectious diseases, genetic disorders, and cancer. The increasing demand for personalized medicine and the continuous development of novel molecular assays for a broader range of conditions are key drivers. The segment is projected to capture approximately 35% of the total IVD market by 2033, with a CAGR of 7.2%. Key drivers include technological advancements in PCR, NGS, and microarrays, alongside increased government funding for infectious disease research and surveillance.

Diagnostic Laboratories: These institutions form the backbone of the IVD market, accounting for over 50% of the market share. Their dominance stems from the high volume of tests performed, the need for sophisticated instrumentation and reagents, and their central role in the healthcare ecosystem. Investment in advanced automation and IT infrastructure further solidifies their position.

Reagents: This product type commands the largest share within the IVD market, estimated at around 60% in 2025. The constant need for consumables for diagnostic tests, coupled with the development of specialized reagent kits for emerging diseases and genetic testing, fuels this segment. Economic policies supporting healthcare infrastructure and research contribute to sustained demand.

Infectious Disease Applications: The persistent threat of infectious diseases, amplified by recent global pandemics, has made this application area the most significant growth driver. Rapid diagnostic solutions for viral, bacterial, and fungal infections are in high demand. The inclusion of COVID-19 test kits in the Australian Register of Therapeutic Goods (ARTG) by Abbott in July 2022 exemplifies the dynamic nature and responsiveness of this segment. Government initiatives for disease prevention and control further bolster this application.

New South Wales (NSW) and Victoria: These states are the dominant geographical regions within Australia, driven by their larger population bases, well-established healthcare infrastructure, and a higher concentration of specialized diagnostic laboratories and research institutions. Significant investment in advanced medical technologies and a robust private healthcare sector further contribute to their market leadership.

Australia In Vitro Diagnostics Market Product Landscape

The Australian IVD product landscape is characterized by rapid innovation and a focus on enhanced diagnostic capabilities. Companies are consistently introducing advanced instruments, such as automated analyzers and point-of-care devices, alongside highly specific and sensitive reagents. Molecular diagnostic kits for detecting infectious diseases like influenza, HIV, and HPV are seeing significant uptake. The development of multiplex assays allows for the simultaneous detection of multiple analytes, improving efficiency and reducing turnaround times. Biodegradable and user-friendly reagent formulations are also emerging. Thermo Fisher Scientific's commitment to developing cutting-edge molecular diagnostic tools and Bio-Rad Laboratories Inc.'s robust portfolio of immuno-assay and molecular testing solutions exemplify the technological advancements driving product performance. These innovations are crucial for improving disease management, enabling early intervention, and personalizing patient care across various applications.

Key Drivers, Barriers & Challenges in Australia In Vitro Diagnostics Market

Key Drivers:

- Technological Advancements: Innovations in molecular diagnostics, immunoassay automation, and AI-powered data analysis are critical growth engines. The development of rapid point-of-care testing solutions is also a significant driver, enhancing accessibility and speed of diagnosis.

- Rising Prevalence of Chronic Diseases: The increasing burden of conditions like diabetes, cancer, and cardiovascular diseases necessitates more frequent and accurate diagnostic testing, boosting market demand.

- Growing Healthcare Expenditure: Increased government and private investment in healthcare infrastructure and services directly translates to higher spending on diagnostic tools and services.

- Focus on Preventative Healthcare: A shift towards proactive health management and early disease detection is driving the adoption of sophisticated diagnostic screening programs.

Barriers & Challenges:

- High Cost of Advanced Technologies: The initial investment in cutting-edge IVD instruments and reagents can be substantial, posing a barrier for smaller healthcare facilities.

- Stringent Regulatory Approvals: Navigating the TGA's approval processes for new diagnostic products can be time-consuming and costly, potentially delaying market entry.

- Reimbursement Policies: Inadequate or complex reimbursement structures for certain IVD tests can impact adoption rates and provider willingness to invest.

- Skilled Workforce Shortages: A lack of trained personnel to operate and interpret results from advanced diagnostic equipment can hinder widespread implementation.

Emerging Opportunities in Australia In Vitro Diagnostics Market

Emerging opportunities in the Australian IVD market lie in the expansion of personalized medicine through advanced genetic testing and companion diagnostics, particularly in oncology. The growing demand for home-use diagnostic kits, driven by convenience and increasing health consciousness, presents a significant untapped market. Furthermore, the integration of AI and big data analytics in IVD offers avenues for predictive diagnostics and improved disease management strategies. Telehealth and remote patient monitoring are also creating opportunities for decentralized diagnostic solutions, expanding access to care in rural and underserved areas. The development of novel diagnostic tools for emerging infectious diseases and antimicrobial resistance monitoring also represents a key growth area.

Growth Accelerators in the Australia In Vitro Diagnostics Market Industry

Growth accelerators in the Australian IVD industry are largely driven by continuous technological breakthroughs, fostering the development of more sensitive, specific, and faster diagnostic methods. Strategic partnerships between IVD manufacturers, research institutions, and healthcare providers are crucial for accelerating the translation of innovation into clinical practice. Market expansion strategies, including the increasing adoption of point-of-care testing and the development of user-friendly home testing kits, are making diagnostics more accessible to a wider population. Furthermore, government initiatives aimed at improving public health outcomes and investing in advanced medical infrastructure are providing a supportive ecosystem for sustained market growth.

Key Players Shaping the Australia In Vitro Diagnostics Market Market

- Abbott

- Thermo Fisher Scientific

- F Hoffmann-La Roche Ltd

- QIAGEN

- Siemens AG

- Becton Dickinson and Company

- Bio-Rad Laboratories Inc

- BioMerieux

Notable Milestones in Australia In Vitro Diagnostics Market Sector

- July 2022: COVID-19 test kits were included in the Australian Register of Therapeutic Goods (ARTG) for legal supply in Australia by Abbott.

- June 2022: CerTest Biotec and BD announced a collaboration to develop a molecular diagnostic test for the monkeypox virus.

In-Depth Australia In Vitro Diagnostics Market Market Outlook

The outlook for the Australian IVD market remains exceptionally positive, underpinned by ongoing technological advancements that are constantly redefining diagnostic capabilities. The increasing integration of AI and automation in diagnostic workflows promises greater efficiency and accuracy. Strategic collaborations, such as the one between CerTest Biotec and BD for monkeypox diagnostics, highlight the industry's proactive stance in addressing emerging health threats. Furthermore, the expanding adoption of point-of-care testing and the burgeoning demand for home-use diagnostic solutions will significantly broaden market reach and accessibility. With a strong focus on personalized medicine and preventative healthcare, the market is poised for sustained growth, offering substantial opportunities for stakeholders to innovate and expand their presence.

Australia In Vitro Diagnostics Market Segmentation

-

1. Test Type

- 1.1. Clinical Chemistry

- 1.2. Molecular Diagnostics

- 1.3. Immuno Diagnostics

- 1.4. Haematology

- 1.5. Other Test Types

-

2. Type of Product

- 2.1. Instruments

- 2.2. Reagents

- 2.3. Other Types of Product

-

3. Application

- 3.1. Infectious Disease

- 3.2. Diabetes

- 3.3. Cancer/Oncology

- 3.4. Cardiology

- 3.5. Autoimmune Disease

- 3.6. Other Applications

-

4. End User

- 4.1. Diagnostic Laboratories

- 4.2. Hospitals and Clinics

- 4.3. Other End Users

Australia In Vitro Diagnostics Market Segmentation By Geography

- 1. Australia

Australia In Vitro Diagnostics Market Regional Market Share

Geographic Coverage of Australia In Vitro Diagnostics Market

Australia In Vitro Diagnostics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.36% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. High Prevalence of Chronic Diseases; Increasing Use of Point-of-care (POC) Diagnostics; Advanced Technologies

- 3.3. Market Restrains

- 3.3.1. Stringent Regulations

- 3.4. Market Trends

- 3.4.1. The Molecular Diagnostics Segment is Expected to Hold a Major Market Share in the Australia In-vitro Diagnostics Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia In Vitro Diagnostics Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Test Type

- 5.1.1. Clinical Chemistry

- 5.1.2. Molecular Diagnostics

- 5.1.3. Immuno Diagnostics

- 5.1.4. Haematology

- 5.1.5. Other Test Types

- 5.2. Market Analysis, Insights and Forecast - by Type of Product

- 5.2.1. Instruments

- 5.2.2. Reagents

- 5.2.3. Other Types of Product

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Infectious Disease

- 5.3.2. Diabetes

- 5.3.3. Cancer/Oncology

- 5.3.4. Cardiology

- 5.3.5. Autoimmune Disease

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Diagnostic Laboratories

- 5.4.2. Hospitals and Clinics

- 5.4.3. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Test Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Becton Dickinson and Company

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 QIAGEN

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Bio-Rad Laboratories Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 F Hoffmann-La Roche Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 BioMerieux

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Siemens AG

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Abbott

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Thermo Fisher Scientific

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.1 Becton Dickinson and Company

List of Figures

- Figure 1: Australia In Vitro Diagnostics Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia In Vitro Diagnostics Market Share (%) by Company 2025

List of Tables

- Table 1: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Test Type 2020 & 2033

- Table 2: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Test Type 2020 & 2033

- Table 3: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Type of Product 2020 & 2033

- Table 4: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Type of Product 2020 & 2033

- Table 5: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Australia In Vitro Diagnostics Market Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 9: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Region 2020 & 2033

- Table 10: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Test Type 2020 & 2033

- Table 12: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Test Type 2020 & 2033

- Table 13: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Type of Product 2020 & 2033

- Table 14: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Type of Product 2020 & 2033

- Table 15: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Application 2020 & 2033

- Table 16: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Application 2020 & 2033

- Table 17: Australia In Vitro Diagnostics Market Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 19: Australia In Vitro Diagnostics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Australia In Vitro Diagnostics Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia In Vitro Diagnostics Market?

The projected CAGR is approximately 5.36%.

2. Which companies are prominent players in the Australia In Vitro Diagnostics Market?

Key companies in the market include Becton Dickinson and Company, QIAGEN, Bio-Rad Laboratories Inc, F Hoffmann-La Roche Ltd, BioMerieux, Siemens AG, Abbott, Thermo Fisher Scientific.

3. What are the main segments of the Australia In Vitro Diagnostics Market?

The market segments include Test Type, Type of Product, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.96 billion as of 2022.

5. What are some drivers contributing to market growth?

High Prevalence of Chronic Diseases; Increasing Use of Point-of-care (POC) Diagnostics; Advanced Technologies.

6. What are the notable trends driving market growth?

The Molecular Diagnostics Segment is Expected to Hold a Major Market Share in the Australia In-vitro Diagnostics Market.

7. Are there any restraints impacting market growth?

Stringent Regulations.

8. Can you provide examples of recent developments in the market?

July 2022: COVID-19 test kits were included in the Australian Register of Therapeutic Goods (ARTG) for legal supply in Australia by Abbott.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia In Vitro Diagnostics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia In Vitro Diagnostics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia In Vitro Diagnostics Market?

To stay informed about further developments, trends, and reports in the Australia In Vitro Diagnostics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence