Key Insights

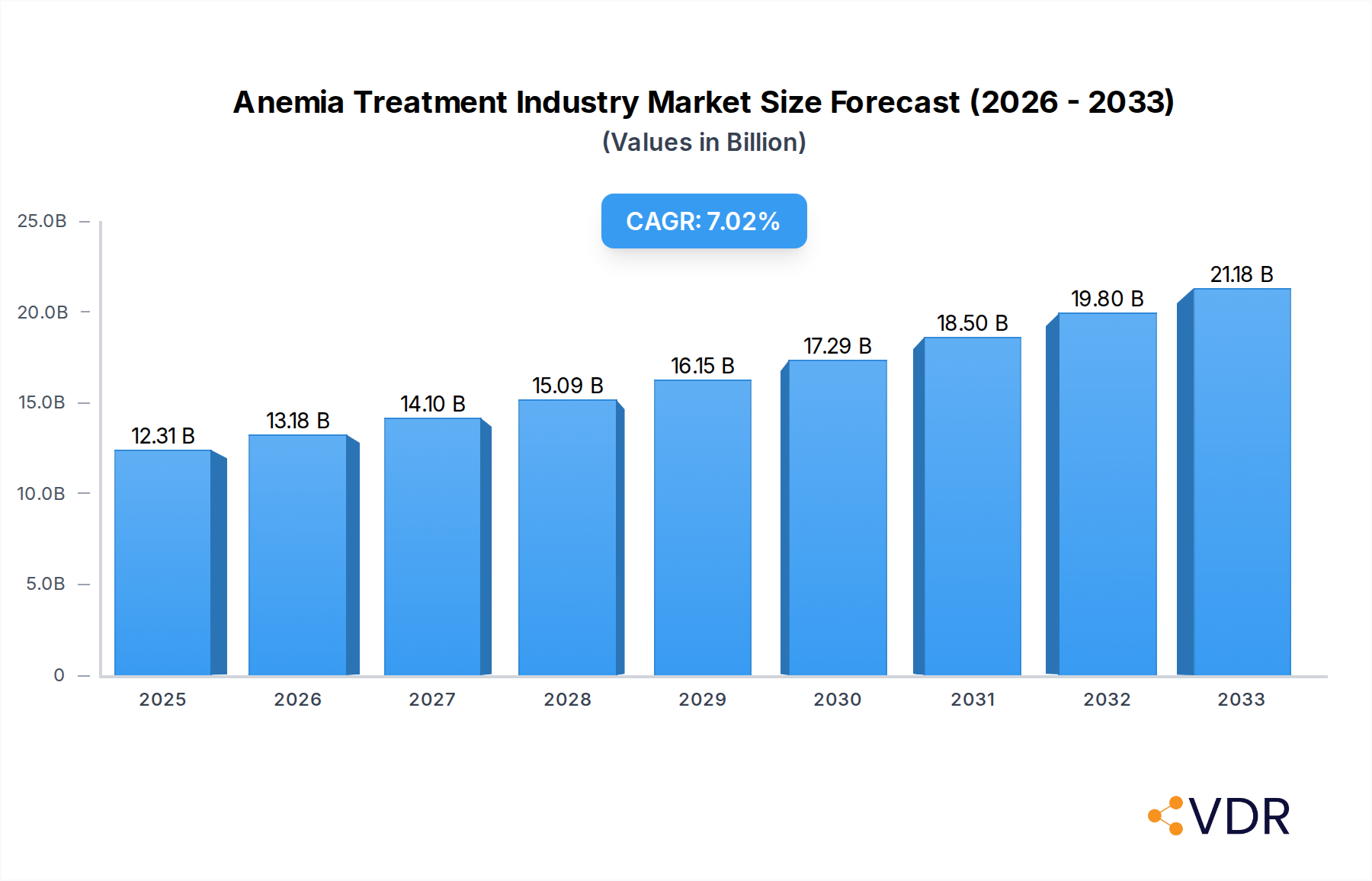

The global Anemia Treatment market is poised for substantial growth, projected to reach $12.31 billion in 2025 and expand at a compelling Compound Annual Growth Rate (CAGR) of 7.12% through 2033. This robust expansion is driven by a confluence of factors, including the increasing prevalence of various anemia types, advancements in diagnostic capabilities leading to earlier detection, and the continuous development of novel therapeutic agents. Iron deficiency anemia remains a significant segment due to its widespread occurrence, particularly in developing nations and among specific demographics like pregnant women and children. Furthermore, the growing incidence of chronic kidney disease (CKD) is a major contributor to the demand for anemia treatments, as CKD-related anemia is a common complication. The market is also witnessing significant innovation in regenerative medicine and gene therapies, offering new avenues for treating complex anemias like sickle cell anemia and aplastic anemia. Increased healthcare expenditure and improved access to medical facilities globally are further fueling market penetration and adoption of advanced treatments.

Anemia Treatment Industry Market Size (In Billion)

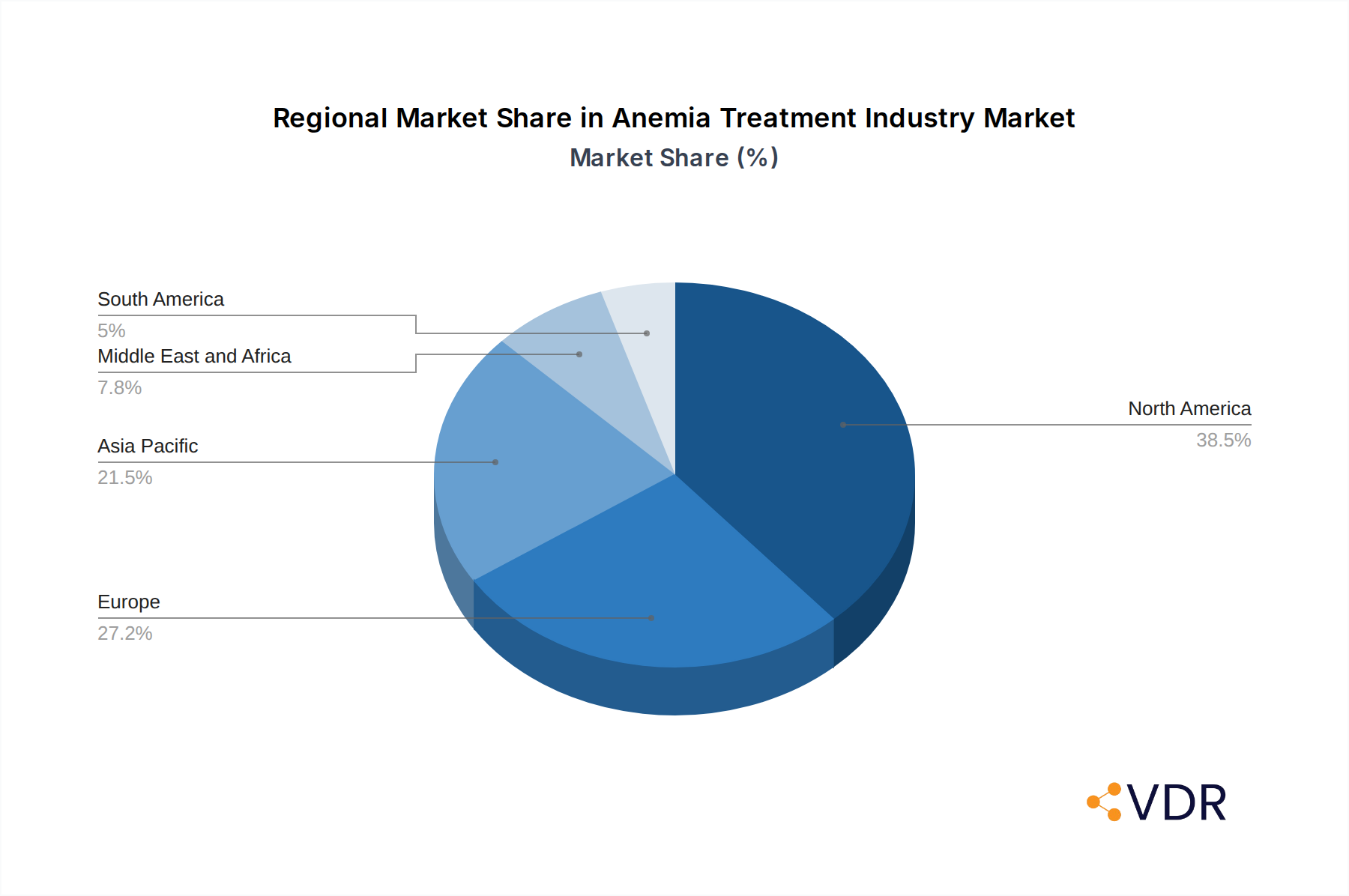

The competitive landscape is characterized by the presence of key pharmaceutical and biotechnology companies actively engaged in research and development, strategic collaborations, and mergers and acquisitions. Companies like Sanofi, Takeda Pharmaceutical Company Limited, and Pfizer Inc. are at the forefront, introducing innovative therapies and expanding their product portfolios. The market is segmented by the type of disease, with Iron Deficiency Anemia and CKD (Chronic Kidney Disease) Anemia holding significant shares, followed by Sickle Cell Anemia, Aplastic Anemia, and Other Diseases. Geographically, North America currently dominates the market, owing to high healthcare spending and advanced medical infrastructure. However, the Asia Pacific region is expected to witness the fastest growth, driven by a large patient pool, increasing awareness, and improving healthcare access. While the market is on an upward trajectory, challenges such as the high cost of newer therapies and the need for stringent regulatory approvals for novel treatments are being addressed through ongoing research and market strategies.

Anemia Treatment Industry Company Market Share

Anemia Treatment Industry: Comprehensive Market Analysis and Forecast 2019–2033

This in-depth report provides a definitive analysis of the global Anemia Treatment Industry, encompassing market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, opportunities, and leading players. With a study period spanning from 2019 to 2033, and a base year of 2025, this report offers critical insights for industry professionals, investors, and stakeholders navigating the evolving anemia treatment market. This analysis covers both parent and child markets, offering a holistic view of market segments and their interdependencies. All values are presented in billions of US dollars.

Anemia Treatment Industry Market Dynamics & Structure

The global Anemia Treatment Industry is characterized by a moderately consolidated market structure, with a few major pharmaceutical companies holding significant market shares. Technological innovation is a primary driver, fueled by ongoing research into novel therapeutic approaches for various anemia types, including Iron Deficiency Anemia (IDA), Chronic Kidney Disease (CKD) Anemia, Sickle Cell Anemia, and Aplastic Anemia. Regulatory frameworks, such as stringent FDA and EMA approvals, significantly influence market entry and product development timelines. Competitive product substitutes, particularly the shift from oral to injectable iron therapies and the emergence of targeted biologics, are reshaping the competitive landscape. End-user demographics, including the aging population and the increasing prevalence of chronic diseases, present a growing demand for effective anemia treatments. Mergers and acquisitions (M&A) remain a key strategy for market expansion and portfolio diversification, with recent years witnessing several strategic consolidations to enhance R&D capabilities and market reach. Barriers to innovation include high R&D costs, lengthy clinical trial processes, and patent expirations.

- Market Concentration: Dominated by a mix of large pharmaceutical corporations and specialized biotechnology firms.

- Technological Innovation: Driven by advancements in drug delivery systems, recombinant erythropoiesis-stimulating agents (ESAs), novel iron formulations, and gene therapies.

- Regulatory Frameworks: Strict approval processes by global health authorities (FDA, EMA, NMPA) shape product pipelines and market access.

- Competitive Product Substitutes: Increasing adoption of intravenous iron, biosimil ESAs, and innovative treatments for specific anemia subtypes.

- End-User Demographics: Rising geriatric population, growing incidence of CKD and cancer, and increased awareness of anemia's impact.

- M&A Trends: Strategic acquisitions and partnerships to gain access to innovative pipelines and expand geographical presence.

- Innovation Barriers: High capital investment for R&D, complex regulatory pathways, and the need for extensive clinical validation.

Anemia Treatment Industry Growth Trends & Insights

The Anemia Treatment Industry is projected to witness robust growth, driven by an increasing global prevalence of anemia and a growing emphasis on better patient outcomes. The market size is expected to evolve significantly from xx billion in 2019 to an estimated $XX billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately XX% between 2025 and 2033. Adoption rates of advanced therapies, particularly for CKD-related anemia and iron deficiency anemia, are on the rise. Technological disruptions, including the development of oral iron chelators and advanced erythropoiesis-stimulating agents (ESAs), are enhancing treatment efficacy and patient convenience. Consumer behavior is shifting towards more proactive health management and a demand for personalized treatment plans, influencing the development of diagnostic tools and tailored therapeutic interventions. Market penetration is expected to deepen as awareness of the long-term health consequences of untreated anemia increases, particularly in emerging economies. The rising incidence of chronic diseases like kidney disease and cancer, which often lead to anemia, further fuels the demand for these treatments.

Dominant Regions, Countries, or Segments in Anemia Treatment Industry

The Iron Deficiency Anemia (IDA) segment is anticipated to remain the dominant force within the Anemia Treatment Industry, driven by its widespread prevalence globally. North America, particularly the United States, currently leads in market share due to high healthcare expenditure, advanced diagnostic capabilities, and a significant patient population with chronic conditions. This dominance is further bolstered by strong government support for medical research and development, coupled with a well-established reimbursement framework for anemia treatments.

Key drivers for IDA's dominance include:

- High Prevalence: IDA is the most common nutritional deficiency worldwide, affecting a substantial portion of the global population, especially women of childbearing age and infants.

- Economic Policies: Favorable healthcare policies and insurance coverage in developed nations ensure greater access to diagnostic tools and treatment options.

- Infrastructure: Robust healthcare infrastructure in North America and Europe facilitates the widespread availability and uptake of various anemia treatment modalities.

- Technological Advancements: The continuous development of more effective and convenient iron replenishment therapies, including novel intravenous iron formulations, caters to a broad patient base.

- Awareness Campaigns: Increased public health initiatives and awareness programs highlight the importance of iron intake and the risks associated with iron deficiency, encouraging early diagnosis and treatment.

While IDA leads, CKD (Chronic Kidney Disease) Anemia is exhibiting significant growth potential, driven by the rising global incidence of kidney disease and the critical need for effective management of anemia in these patients. Sickle Cell Anemia and Aplastic Anemia, though rarer, represent specialized markets with high unmet needs and potential for advanced therapeutic interventions.

Anemia Treatment Industry Product Landscape

The Anemia Treatment Industry's product landscape is marked by significant innovation, with a focus on enhancing efficacy, safety, and patient convenience. Key product categories include iron supplements (oral and intravenous), erythropoiesis-stimulating agents (ESAs), vitamin B12 and folate supplements, and emerging biologics and gene therapies. Intravenous iron formulations, such as ferric carboxymaltose, are gaining traction due to their rapid replenishment capabilities and improved patient adherence compared to some oral alternatives. ESAs are crucial for managing anemia in CKD patients, with ongoing research aimed at developing agents with improved safety profiles and targeted mechanisms of action. The development of novel treatments for rare anemias, like cold agglutinin disease (CAD), showcases the industry's commitment to addressing diverse and unmet medical needs. Technological advancements are also focusing on companion diagnostics and personalized treatment approaches to optimize therapeutic outcomes.

Key Drivers, Barriers & Challenges in Anemia Treatment Industry

Key Drivers:

- Rising Prevalence of Anemia: Increasing incidence of chronic diseases like CKD, cancer, and gastrointestinal disorders, which are major causes of anemia.

- Technological Advancements: Development of novel therapeutic agents, improved drug delivery systems, and personalized medicine approaches.

- Growing Healthcare Expenditure: Increased investment in healthcare infrastructure and R&D globally, particularly in emerging markets.

- Awareness and Diagnosis: Growing awareness among patients and healthcare providers about the symptoms and long-term consequences of anemia.

Barriers & Challenges:

- High R&D Costs: Significant investment required for drug discovery, clinical trials, and regulatory approvals.

- Stringent Regulatory Hurdles: Lengthy and complex approval processes by health authorities worldwide.

- Competition from Generics and Biosimilars: Pressure on pricing and market share from off-patent products.

- Reimbursement Policies: Variations in reimbursement policies across different regions can affect market access and affordability.

- Supply Chain Disruptions: Potential for disruptions in the supply of raw materials and finished products.

Emerging Opportunities in Anemia Treatment Industry

Emerging opportunities in the Anemia Treatment Industry lie in the development of advanced therapies for rare anemias, such as those requiring novel biologics or gene therapies for conditions like sickle cell disease and certain autoimmune anemias. The increasing focus on patient-centric care is driving innovation in oral iron formulations with enhanced bioavailability and reduced gastrointestinal side effects. Furthermore, the growing prevalence of anemia in aging populations and in patients with chronic inflammatory conditions presents a substantial opportunity for more targeted and effective treatment strategies. The integration of AI and machine learning in drug discovery and diagnostics also holds promise for identifying new therapeutic targets and personalizing treatment regimens, leading to improved patient outcomes and market expansion.

Growth Accelerators in the Anemia Treatment Industry Industry

Several catalysts are accelerating growth in the Anemia Treatment Industry. Continuous innovation in erythropoiesis-stimulating agents (ESAs) and iron replacement therapies, with a focus on improved safety profiles and patient convenience, is a key accelerator. Strategic partnerships and collaborations between pharmaceutical companies, research institutions, and biotechnology firms are fostering R&D pipelines and expediting the launch of new treatments. Market expansion into emerging economies, driven by increasing healthcare infrastructure and rising disposable incomes, is another significant growth driver. Furthermore, the growing understanding of the multifactorial nature of anemia and its impact on overall health is prompting greater investment in comprehensive treatment solutions, including preventative measures and combination therapies.

Key Players Shaping the Anemia Treatment Industry Market

- Covis Pharma GmbH (AMAG Pharmaceuticals Inc)

- Sanofi

- Pieris Pharmaceuticals Inc

- Akebia Therapeutics Inc

- Takeda Pharmaceutical Company Limited

- Pharmacosmos A/S

- GSK plc

- Bluebird Bio Inc

- AbbVie Inc (Allergan Plc)

- Pfizer Inc (Global Blood Therapeutics Inc)

Notable Milestones in Anemia Treatment Industry Sector

- November 2022: Sanofi received approval from the European Commission (EC) for Enjaymo (sutimlimab) for the treatment of hemolytic anemia in adult patients with cold agglutinin disease (CAD). This approval marks a significant advancement in treating a rare, chronic autoimmune hemolytic anemia.

- November 2022: CSL Vifor and Fresenius Kabi received approval from China's National NMPA for its Ferinject (ferric carboxymaltose). This approval expands the availability of intravenous iron therapy for iron deficiency in adult patients where oral iron is ineffective or rapid iron delivery is clinically needed.

In-Depth Anemia Treatment Industry Market Outlook

The Anemia Treatment Industry is poised for significant future growth, driven by ongoing advancements in therapeutic modalities and an increasing global demand for effective anemia management. The outlook is particularly bright for novel biologics targeting specific anemia subtypes and for innovative iron replacement therapies that offer improved patient adherence and outcomes. Strategic partnerships and market expansion initiatives in emerging economies will play a crucial role in unlocking new revenue streams and broadening access to essential treatments. The industry's focus on personalized medicine and the integration of digital health solutions will further enhance treatment efficacy and patient engagement, creating a more dynamic and responsive market landscape for the forecast period.

Anemia Treatment Industry Segmentation

-

1. Type of Disease

- 1.1. Iron Deficiency Anemia

- 1.2. CKD (Chronic Kidney Disease) Anemia

- 1.3. Sickle Cell Anemia

- 1.4. Aplastic Anemia

- 1.5. Other Diseases

Anemia Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Anemia Treatment Industry Regional Market Share

Geographic Coverage of Anemia Treatment Industry

Anemia Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Disease

- 5.1.1. Iron Deficiency Anemia

- 5.1.2. CKD (Chronic Kidney Disease) Anemia

- 5.1.3. Sickle Cell Anemia

- 5.1.4. Aplastic Anemia

- 5.1.5. Other Diseases

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Middle East and Africa

- 5.2.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type of Disease

- 6. Global Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Disease

- 6.1.1. Iron Deficiency Anemia

- 6.1.2. CKD (Chronic Kidney Disease) Anemia

- 6.1.3. Sickle Cell Anemia

- 6.1.4. Aplastic Anemia

- 6.1.5. Other Diseases

- 6.1. Market Analysis, Insights and Forecast - by Type of Disease

- 7. North America Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type of Disease

- 7.1.1. Iron Deficiency Anemia

- 7.1.2. CKD (Chronic Kidney Disease) Anemia

- 7.1.3. Sickle Cell Anemia

- 7.1.4. Aplastic Anemia

- 7.1.5. Other Diseases

- 7.1. Market Analysis, Insights and Forecast - by Type of Disease

- 8. Europe Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type of Disease

- 8.1.1. Iron Deficiency Anemia

- 8.1.2. CKD (Chronic Kidney Disease) Anemia

- 8.1.3. Sickle Cell Anemia

- 8.1.4. Aplastic Anemia

- 8.1.5. Other Diseases

- 8.1. Market Analysis, Insights and Forecast - by Type of Disease

- 9. Asia Pacific Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type of Disease

- 9.1.1. Iron Deficiency Anemia

- 9.1.2. CKD (Chronic Kidney Disease) Anemia

- 9.1.3. Sickle Cell Anemia

- 9.1.4. Aplastic Anemia

- 9.1.5. Other Diseases

- 9.1. Market Analysis, Insights and Forecast - by Type of Disease

- 10. Middle East and Africa Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type of Disease

- 10.1.1. Iron Deficiency Anemia

- 10.1.2. CKD (Chronic Kidney Disease) Anemia

- 10.1.3. Sickle Cell Anemia

- 10.1.4. Aplastic Anemia

- 10.1.5. Other Diseases

- 10.1. Market Analysis, Insights and Forecast - by Type of Disease

- 11. South America Anemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type of Disease

- 11.1.1. Iron Deficiency Anemia

- 11.1.2. CKD (Chronic Kidney Disease) Anemia

- 11.1.3. Sickle Cell Anemia

- 11.1.4. Aplastic Anemia

- 11.1.5. Other Diseases

- 11.1. Market Analysis, Insights and Forecast - by Type of Disease

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Covis Pharma GmbH (AMAG Pharmaceuticals Inc )

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sanofi

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Pieris Pharmaceuticals Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Akebia Therapeutics Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Takeda Pharmaceutical Company Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pharmacosmos A/S

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 GSK plc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bluebird Bio Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 AbbVie Inc (Allergan Plc)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Pfizer Inc (Global Blood Therapeutics Inc )

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Covis Pharma GmbH (AMAG Pharmaceuticals Inc )

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Anemia Treatment Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Anemia Treatment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Anemia Treatment Industry Revenue (billion), by Type of Disease 2025 & 2033

- Figure 4: North America Anemia Treatment Industry Volume (K Unit), by Type of Disease 2025 & 2033

- Figure 5: North America Anemia Treatment Industry Revenue Share (%), by Type of Disease 2025 & 2033

- Figure 6: North America Anemia Treatment Industry Volume Share (%), by Type of Disease 2025 & 2033

- Figure 7: North America Anemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: North America Anemia Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 9: North America Anemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Anemia Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Anemia Treatment Industry Revenue (billion), by Type of Disease 2025 & 2033

- Figure 12: Europe Anemia Treatment Industry Volume (K Unit), by Type of Disease 2025 & 2033

- Figure 13: Europe Anemia Treatment Industry Revenue Share (%), by Type of Disease 2025 & 2033

- Figure 14: Europe Anemia Treatment Industry Volume Share (%), by Type of Disease 2025 & 2033

- Figure 15: Europe Anemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Europe Anemia Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: Europe Anemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Anemia Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Anemia Treatment Industry Revenue (billion), by Type of Disease 2025 & 2033

- Figure 20: Asia Pacific Anemia Treatment Industry Volume (K Unit), by Type of Disease 2025 & 2033

- Figure 21: Asia Pacific Anemia Treatment Industry Revenue Share (%), by Type of Disease 2025 & 2033

- Figure 22: Asia Pacific Anemia Treatment Industry Volume Share (%), by Type of Disease 2025 & 2033

- Figure 23: Asia Pacific Anemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Asia Pacific Anemia Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Asia Pacific Anemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Anemia Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Middle East and Africa Anemia Treatment Industry Revenue (billion), by Type of Disease 2025 & 2033

- Figure 28: Middle East and Africa Anemia Treatment Industry Volume (K Unit), by Type of Disease 2025 & 2033

- Figure 29: Middle East and Africa Anemia Treatment Industry Revenue Share (%), by Type of Disease 2025 & 2033

- Figure 30: Middle East and Africa Anemia Treatment Industry Volume Share (%), by Type of Disease 2025 & 2033

- Figure 31: Middle East and Africa Anemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Middle East and Africa Anemia Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Middle East and Africa Anemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Anemia Treatment Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: South America Anemia Treatment Industry Revenue (billion), by Type of Disease 2025 & 2033

- Figure 36: South America Anemia Treatment Industry Volume (K Unit), by Type of Disease 2025 & 2033

- Figure 37: South America Anemia Treatment Industry Revenue Share (%), by Type of Disease 2025 & 2033

- Figure 38: South America Anemia Treatment Industry Volume Share (%), by Type of Disease 2025 & 2033

- Figure 39: South America Anemia Treatment Industry Revenue (billion), by Country 2025 & 2033

- Figure 40: South America Anemia Treatment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 41: South America Anemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Anemia Treatment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 2: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 3: Global Anemia Treatment Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Anemia Treatment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 5: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 6: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 7: Global Anemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Anemia Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 9: United States Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: United States Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 11: Canada Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 13: Mexico Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Mexico Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 16: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 17: Global Anemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Anemia Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 19: Germany Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: France Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Italy Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Italy Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Spain Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Spain Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 32: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 33: Global Anemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Global Anemia Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 35: China Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: China Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Japan Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Japan Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: India Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: India Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Australia Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Australia Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: South Korea Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: South Korea Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Rest of Asia Pacific Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 48: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 49: Global Anemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Anemia Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: GCC Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: GCC Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: South Africa Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: South Africa Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Rest of Middle East and Africa Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East and Africa Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Global Anemia Treatment Industry Revenue billion Forecast, by Type of Disease 2020 & 2033

- Table 58: Global Anemia Treatment Industry Volume K Unit Forecast, by Type of Disease 2020 & 2033

- Table 59: Global Anemia Treatment Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Anemia Treatment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Brazil Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Brazil Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Argentina Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Argentina Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of South America Anemia Treatment Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Rest of South America Anemia Treatment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Anemia Treatment Industry?

The projected CAGR is approximately 7.12%.

2. Which companies are prominent players in the Anemia Treatment Industry?

Key companies in the market include Covis Pharma GmbH (AMAG Pharmaceuticals Inc ), Sanofi, Pieris Pharmaceuticals Inc, Akebia Therapeutics Inc, Takeda Pharmaceutical Company Limited, Pharmacosmos A/S, GSK plc, Bluebird Bio Inc, AbbVie Inc (Allergan Plc), Pfizer Inc (Global Blood Therapeutics Inc ).

3. What are the main segments of the Anemia Treatment Industry?

The market segments include Type of Disease.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.31 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Cases of Anemia Across the Globe; Increasing Number of Women With Reproductive Age.

6. What are the notable trends driving market growth?

Iron Deficiency Anemia to Witness Healthy Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Awareness About the Treatment in Developing Regions; High Cost of Drugs.

8. Can you provide examples of recent developments in the market?

November 2022: Sanofi received approval from the European Commission (EC) for Enjaymo (sutimlimab) for the treatment of hemolytic anemia in adult patients with cold agglutinin disease (CAD), a rare, serious, and chronic autoimmune hemolytic anemia, where the body's immune system mistakenly attacks healthy red blood cells and causes their rupture, known as hemolysis.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Anemia Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Anemia Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Anemia Treatment Industry?

To stay informed about further developments, trends, and reports in the Anemia Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence