Key Insights

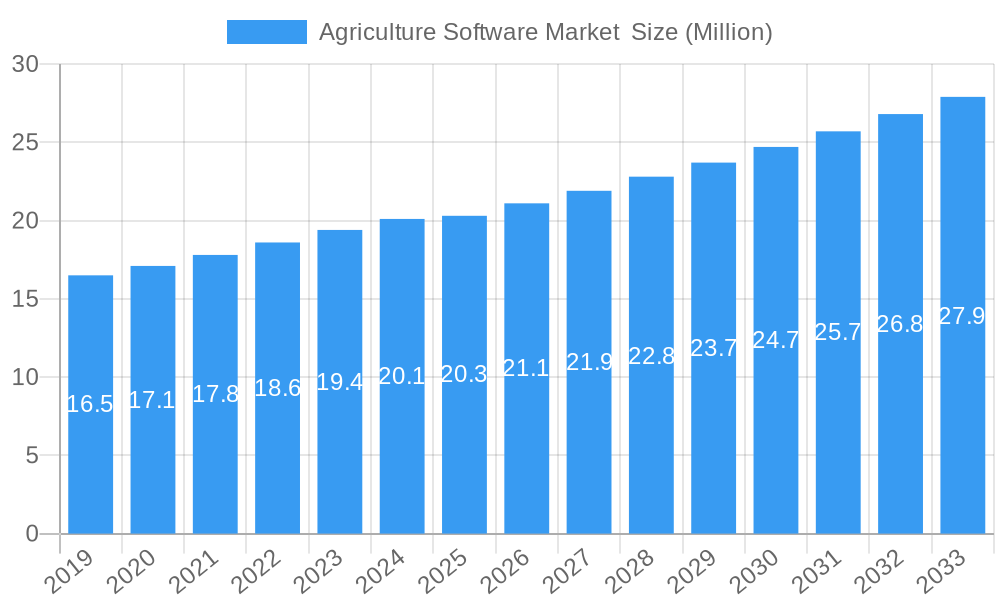

The global Agriculture Software Market is poised for robust growth, projected to reach an estimated USD 20.3 billion by 2025, with a significant Compound Annual Growth Rate (CAGR) of 4.2% through 2033. This expansion is primarily driven by the increasing adoption of advanced technologies to enhance agricultural efficiency, sustainability, and profitability. Key growth catalysts include the escalating need for data-driven decision-making in farming operations, precision agriculture techniques to optimize resource utilization (water, fertilizers, pesticides), and the burgeoning demand for real-time monitoring and management solutions for livestock and crops. The digital transformation within the agricultural sector is accelerating, with farmers and agricultural enterprises embracing software solutions to improve yields, reduce operational costs, and navigate complex environmental challenges. The market is witnessing a strong shift towards cloud-based solutions, including Software-as-a-Service (SaaS) and Platform-as-a-Service (PaaS), due to their scalability, accessibility, and cost-effectiveness compared to traditional on-premise systems. This trend facilitates easier integration of various agricultural technologies and provides valuable insights from vast datasets.

Agriculture Software Market Market Size (In Million)

Further propelling this market are innovations in smart farming technologies such as IoT sensors, AI-powered analytics, and drone technology, all of which rely heavily on sophisticated software platforms. Precision farming, livestock tracking and monitoring, and smart greenhouse applications represent major segments capitalizing on these advancements. While the market is characterized by strong growth potential, certain restraints exist. These include the high initial investment costs associated with some advanced agricultural software and hardware, a potential lack of digital literacy among a segment of the farming community, and concerns regarding data security and privacy. However, the long-term outlook remains highly optimistic, supported by government initiatives promoting agricultural modernization, increasing awareness of sustainable farming practices, and the continuous innovation by key players like Deere & Company, Oracle, and Trimble Inc. These companies are at the forefront of developing integrated solutions that address the evolving needs of the modern agricultural landscape.

Agriculture Software Market Company Market Share

Here is a compelling, SEO-optimized report description for the Agriculture Software Market, designed to maximize search engine visibility and engage industry professionals, with no placeholders and values presented in billions.

Unlocking Precision and Profitability: The Global Agriculture Software Market Report

Gain unparalleled insights into the rapidly evolving global Agriculture Software Market with this comprehensive, data-driven report. From precision farming innovations to smart greenhouse management, this study dissects the technologies and strategies revolutionizing modern agriculture. Understand market dynamics, growth trajectories, and key player contributions to inform your business decisions and capitalize on emerging opportunities in this vital sector. This report forecasts the agriculture software market size to reach $XX billion by 2033, expanding at a CAGR of XX% during the forecast period.

Agriculture Software Market Market Dynamics & Structure

The agriculture software market is characterized by a dynamic interplay of technological advancement, evolving regulatory landscapes, and increasing demand for operational efficiency. Market concentration is moderately fragmented, with both established giants and agile startups vying for market share. Technological innovation is primarily driven by the need for enhanced crop yields, reduced resource consumption, and improved sustainability. Key drivers include the proliferation of IoT devices, advancements in AI and machine learning for data analysis, and the increasing accessibility of cloud-based solutions. Regulatory frameworks, particularly those concerning data privacy and environmental impact, are becoming increasingly influential, shaping the development and adoption of new software. Competitive product substitutes, while present in the form of traditional farming methods, are rapidly being overshadowed by the demonstrable benefits of digital solutions. End-user demographics are broadening, encompassing large-scale commercial farms, medium-sized operations, and increasingly, smallholder farmers seeking to leverage technology for growth. Mergers and acquisitions (M&A) are a significant trend, with larger players acquiring innovative startups to expand their product portfolios and technological capabilities. For instance, the historical period saw numerous strategic acquisitions aimed at consolidating market presence and integrating diverse functionalities.

- Market Concentration: Moderately fragmented with a mix of large enterprises and niche players.

- Technological Innovation Drivers: IoT, AI/ML, Cloud Computing, Big Data Analytics.

- Regulatory Frameworks: Data privacy, environmental compliance, agricultural subsidies.

- Competitive Product Substitutes: Traditional manual farming, basic farm management tools.

- End-User Demographics: Commercial farms, medium-sized farms, smallholder farmers, agricultural cooperatives.

- M&A Trends: Consolidating market share, acquiring specialized technologies, expanding service offerings.

Agriculture Software Market Growth Trends & Insights

The global agriculture software market is poised for robust expansion, driven by an escalating need for data-driven decision-making and operational optimization across the agricultural value chain. The market size evolution is marked by a consistent upward trajectory, fueled by increasing investments in precision agriculture technologies and the adoption of cloud-based Software-as-a-Service (SaaS) models. These adoption rates are accelerating as farmers recognize the tangible benefits of reduced input costs, improved yield quality, and enhanced resource management. Technological disruptions are at the forefront of this growth, with advancements in artificial intelligence (AI), machine learning (ML), the Internet of Things (IoT), and drone technology enabling more sophisticated data collection and analysis. These innovations are transforming traditional farming practices into highly efficient, predictive, and responsive operations. Consumer behavior shifts are also playing a crucial role, with a growing demand for sustainably produced food and greater transparency in food supply chains, compelling farmers to adopt technologies that can provide verifiable data on their practices.

The market penetration of advanced agriculture software is expanding beyond large commercial entities to smaller and medium-sized farms, facilitated by more accessible pricing models and user-friendly interfaces. The estimated market size for agriculture software in 2025 is projected to be $XX billion, with projections indicating a significant increase to $XX billion by 2033. This growth is underpinned by a compound annual growth rate (CAGR) of approximately XX% between 2025 and 2033. The increasing integration of different software applications, creating holistic farm management systems, further accelerates market adoption. These systems offer a unified platform for tasks ranging from crop planning and monitoring to financial management and supply chain logistics. Furthermore, government initiatives and subsidies aimed at promoting digital agriculture and sustainable farming practices are acting as significant catalysts for market growth. The ability of agriculture software to provide actionable insights from vast amounts of data collected from sensors, drones, and satellite imagery is a key factor driving its increasing relevance and adoption. The focus is shifting from basic record-keeping to predictive analytics, enabling farmers to anticipate challenges like pest outbreaks, disease, and adverse weather conditions, and to take proactive measures to mitigate their impact. The integration of technologies like blockchain for enhanced traceability and supply chain integrity is also emerging as a significant trend.

Dominant Regions, Countries, or Segments in Agriculture Software Market

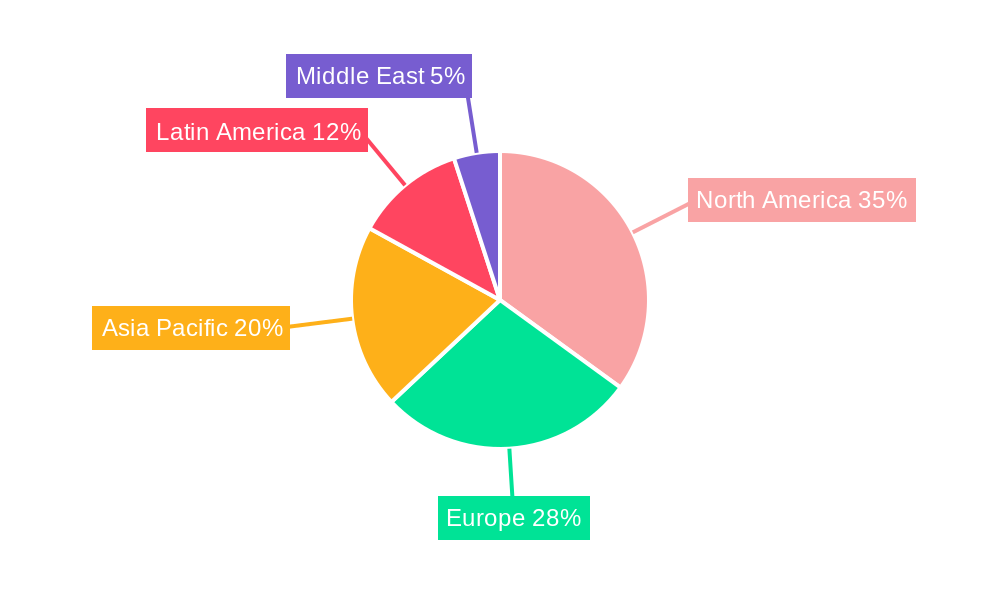

North America currently stands as the dominant region in the global agriculture software market, driven by its advanced agricultural infrastructure, high adoption rates of precision farming technologies, and significant investment in agricultural research and development. The United States, in particular, leads in this region due to its large-scale commercial farms, early embrace of technological solutions, and robust government support for agricultural innovation. The extensive use of Precision Farming applications, a key segment within the agriculture software market, is a primary driver of this regional dominance. These applications leverage GPS technology, sensors, and data analytics to optimize planting, fertilization, irrigation, and pest control, leading to increased yields and reduced resource wastage. The market share within North America for precision farming software is estimated to be a substantial XX% of the total regional software expenditure.

The widespread adoption of Cloud-based deployment types, particularly Software-as-a-Service (SaaS), is another significant factor contributing to North America's leadership. Cloud solutions offer scalability, accessibility, and cost-effectiveness, making them attractive to a broad spectrum of agricultural enterprises. The market penetration of cloud-based agriculture software in North America is projected to exceed XX% by 2025. Countries like Canada also contribute to this regional dominance through their progressive agricultural policies and increasing adoption of smart farming techniques. The economic policies in these countries, which often include incentives for technology adoption and sustainable farming practices, further bolster the growth of the agriculture software market.

Beyond North America, Europe represents another significant market, driven by the European Union's Common Agricultural Policy (CAP) which encourages modernization and sustainability. Germany, France, and the UK are key contributors to the European market, with a growing focus on Livestock Tracking and Monitoring software, contributing approximately XX% of the European agriculture software market. Asia-Pacific is emerging as a high-growth region, fueled by the large agricultural base, increasing internet penetration, and government initiatives to boost food production through technology. Countries like China and India are witnessing rapid adoption of mobile-based agricultural applications and precision farming tools. The growth potential in these developing economies is immense, with market penetration expected to surge in the coming years. The Smart Greenhouse segment, while currently smaller, is experiencing rapid growth globally, driven by the demand for controlled environment agriculture and year-round production, particularly in regions with challenging climates. Precision Forestry is also gaining traction, especially in regions with extensive forest management operations.

Agriculture Software Market Product Landscape

The agriculture software market is defined by a rich and diverse product landscape designed to address specific needs within modern farming operations. Key innovations include integrated farm management systems that consolidate data from various sources for comprehensive oversight. Precision farming software offers advanced analytics for optimized input application, while livestock tracking solutions utilize IoT sensors for real-time monitoring of animal health and welfare. Smart greenhouse software enables precise control of environmental conditions to maximize crop yields. Performance metrics consistently highlight improved efficiency, reduced operational costs, and enhanced crop quality as primary benefits. Unique selling propositions often revolve around data visualization tools, predictive analytics capabilities, and seamless integration with existing farm equipment. Technological advancements are continuously enhancing the accuracy of data collection through sophisticated sensor networks and AI-powered analysis.

Key Drivers, Barriers & Challenges in Agriculture Software Market

The agriculture software market is propelled by several key drivers. The increasing global population necessitates enhanced food production efficiency, driving demand for advanced farming technologies. Technological advancements in areas like IoT, AI, and data analytics provide the tools to achieve this. Furthermore, growing environmental concerns and the need for sustainable farming practices encourage the adoption of software that optimizes resource utilization and minimizes waste. Government initiatives and subsidies promoting digital agriculture also play a crucial role.

However, the market faces significant barriers and challenges. High upfront investment costs for implementing sophisticated software systems can be a deterrent for smaller farms. A lack of digital literacy and the perceived complexity of some software solutions can hinder adoption. Inadequate internet infrastructure in certain rural areas also presents a challenge. Supply chain disruptions can impact the availability of hardware components crucial for some software applications. Moreover, data security and privacy concerns among farmers need to be addressed effectively. Intense competition among software providers can also lead to pricing pressures.

Emerging Opportunities in Agriculture Software Market

Emerging opportunities in the agriculture software market are abundant, driven by evolving consumer demands and technological breakthroughs. The increasing focus on sustainable and organic farming practices creates a demand for specialized software that can monitor and verify these methods, along with solutions for carbon footprint tracking and management. The growth of vertical farming and controlled environment agriculture presents a significant opportunity for smart greenhouse and indoor farming management software. Furthermore, the untapped potential in developing economies, particularly in Africa and Southeast Asia, offers substantial growth prospects as these regions increasingly embrace agricultural technology to enhance food security and farmer livelihoods. The development of AI-powered predictive analytics for disease and pest outbreak prediction, and hyper-personalized farming recommendations based on granular data, represent further avenues for innovation and market expansion.

Growth Accelerators in the Agriculture Software Market Industry

The long-term growth of the agriculture software market is significantly accelerated by groundbreaking technological advancements, strategic partnerships, and expansive market strategies. The continued evolution of AI and machine learning algorithms, enabling more accurate predictive analytics and automated decision-making, is a major catalyst. Strategic partnerships between software providers, agricultural equipment manufacturers, and agronomical research institutions are crucial for developing integrated solutions and expanding market reach. Furthermore, the increasing focus on data integration and interoperability across different platforms will facilitate a more seamless and efficient digital farming ecosystem. Market expansion strategies, including the development of tailored solutions for specific crop types or farming scales and entry into underserved geographic regions, will also fuel sustained growth.

Key Players Shaping the Agriculture Software Market Market

- Farmbrite

- Deere & Company

- AgJunction Inc

- Topcon Corporation

- AGCO Corporation

- Conservis

- AGRIVI Ltd

- Oracle Corporation

- Trimble Inc

- Ag Leader Technology Incorporated

- Raven Industries Inc

Notable Milestones in Agriculture Software Market Sector

- April 2023: CropX, a provider of decision and planning tools, secured a Series C financing round with USD 30 million to advance its farm management system, integrating data from the earth and the sky to provide soil and crop intelligence.

- February 2023: Topcon Corporation launched a solution for specialized farmers called Transplanting Control. The growers of permanent and perennial trees, fruits, and vegetable crops can profit from this system, which provides GNSS-based guiding, autosteering, and control, designed to reduce labor costs, boost productivity, and increase efficiency.

In-Depth Agriculture Software Market Market Outlook

The future outlook for the agriculture software market is exceptionally promising, driven by the relentless pursuit of efficiency, sustainability, and profitability in global food production. Growth accelerators, including the ubiquitous integration of AI for predictive analytics, the expansion of cloud-based platforms, and the increasing adoption of IoT devices for real-time data capture, are set to redefine farming operations. Strategic alliances between technology providers and agricultural stakeholders will foster innovation and create comprehensive, end-to-end solutions. The market's future potential lies in its ability to empower farmers with unprecedented insights, enabling them to navigate complex environmental and economic challenges while meeting the escalating global demand for food. Key strategic opportunities include developing highly personalized farm management plans, enhancing supply chain traceability through blockchain technology, and expanding access to advanced digital tools in emerging agricultural economies.

Agriculture Software Market Segmentation

-

1. Deployment Type

-

1.1. Cloud

- 1.1.1. Software-as-a-service (SAAS)

- 1.1.2. Platform-as-a-service (PAAS)

- 1.2. On-premise

-

1.1. Cloud

-

2. Application

- 2.1. Precision Farming

- 2.2. Livestock Tracking and Monitoring

- 2.3. Smart Greenhouse

- 2.4. Precision Forestry

- 2.5. Other Applications

Agriculture Software Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Australia and New Zealand

- 3.3. Thailand

- 3.4. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Mexico

- 4.3. Argentina

- 4.4. Rest of Latin America

- 5. Middle East

Agriculture Software Market Regional Market Share

Geographic Coverage of Agriculture Software Market

Agriculture Software Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 5.1.1. Cloud

- 5.1.1.1. Software-as-a-service (SAAS)

- 5.1.1.2. Platform-as-a-service (PAAS)

- 5.1.2. On-premise

- 5.1.1. Cloud

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Precision Farming

- 5.2.2. Livestock Tracking and Monitoring

- 5.2.3. Smart Greenhouse

- 5.2.4. Precision Forestry

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6. Global Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 6.1.1. Cloud

- 6.1.1.1. Software-as-a-service (SAAS)

- 6.1.1.2. Platform-as-a-service (PAAS)

- 6.1.2. On-premise

- 6.1.1. Cloud

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Precision Farming

- 6.2.2. Livestock Tracking and Monitoring

- 6.2.3. Smart Greenhouse

- 6.2.4. Precision Forestry

- 6.2.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7. North America Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 7.1.1. Cloud

- 7.1.1.1. Software-as-a-service (SAAS)

- 7.1.1.2. Platform-as-a-service (PAAS)

- 7.1.2. On-premise

- 7.1.1. Cloud

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Precision Farming

- 7.2.2. Livestock Tracking and Monitoring

- 7.2.3. Smart Greenhouse

- 7.2.4. Precision Forestry

- 7.2.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8. Europe Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 8.1.1. Cloud

- 8.1.1.1. Software-as-a-service (SAAS)

- 8.1.1.2. Platform-as-a-service (PAAS)

- 8.1.2. On-premise

- 8.1.1. Cloud

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Precision Farming

- 8.2.2. Livestock Tracking and Monitoring

- 8.2.3. Smart Greenhouse

- 8.2.4. Precision Forestry

- 8.2.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9. Asia Pacific Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 9.1.1. Cloud

- 9.1.1.1. Software-as-a-service (SAAS)

- 9.1.1.2. Platform-as-a-service (PAAS)

- 9.1.2. On-premise

- 9.1.1. Cloud

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Precision Farming

- 9.2.2. Livestock Tracking and Monitoring

- 9.2.3. Smart Greenhouse

- 9.2.4. Precision Forestry

- 9.2.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10. Latin America Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 10.1.1. Cloud

- 10.1.1.1. Software-as-a-service (SAAS)

- 10.1.1.2. Platform-as-a-service (PAAS)

- 10.1.2. On-premise

- 10.1.1. Cloud

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Precision Farming

- 10.2.2. Livestock Tracking and Monitoring

- 10.2.3. Smart Greenhouse

- 10.2.4. Precision Forestry

- 10.2.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11. Middle East Agriculture Software Market Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 11.1.1. Cloud

- 11.1.1.1. Software-as-a-service (SAAS)

- 11.1.1.2. Platform-as-a-service (PAAS)

- 11.1.2. On-premise

- 11.1.1. Cloud

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Precision Farming

- 11.2.2. Livestock Tracking and Monitoring

- 11.2.3. Smart Greenhouse

- 11.2.4. Precision Forestry

- 11.2.5. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Deployment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Farmbrite

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Deere & Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 AgJunction Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Topcon Corporation*List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 AGCO Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Conservis

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 AGRIVI Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oracle Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Trimble Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ag Leader Technology Incorporated

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Raven Industries Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Farmbrite

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Agriculture Software Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Agriculture Software Market Revenue (billion), by Deployment Type 2025 & 2033

- Figure 3: North America Agriculture Software Market Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 4: North America Agriculture Software Market Revenue (billion), by Application 2025 & 2033

- Figure 5: North America Agriculture Software Market Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Agriculture Software Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Agriculture Software Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Agriculture Software Market Revenue (billion), by Deployment Type 2025 & 2033

- Figure 9: Europe Agriculture Software Market Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 10: Europe Agriculture Software Market Revenue (billion), by Application 2025 & 2033

- Figure 11: Europe Agriculture Software Market Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Agriculture Software Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Agriculture Software Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Agriculture Software Market Revenue (billion), by Deployment Type 2025 & 2033

- Figure 15: Asia Pacific Agriculture Software Market Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 16: Asia Pacific Agriculture Software Market Revenue (billion), by Application 2025 & 2033

- Figure 17: Asia Pacific Agriculture Software Market Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Agriculture Software Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Agriculture Software Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Agriculture Software Market Revenue (billion), by Deployment Type 2025 & 2033

- Figure 21: Latin America Agriculture Software Market Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 22: Latin America Agriculture Software Market Revenue (billion), by Application 2025 & 2033

- Figure 23: Latin America Agriculture Software Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: Latin America Agriculture Software Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Agriculture Software Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Agriculture Software Market Revenue (billion), by Deployment Type 2025 & 2033

- Figure 27: Middle East Agriculture Software Market Revenue Share (%), by Deployment Type 2025 & 2033

- Figure 28: Middle East Agriculture Software Market Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East Agriculture Software Market Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East Agriculture Software Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East Agriculture Software Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 2: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Agriculture Software Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 5: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Agriculture Software Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 10: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Agriculture Software Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Germany Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 17: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global Agriculture Software Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: China Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Australia and New Zealand Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Thailand Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 24: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Agriculture Software Market Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Brazil Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Mexico Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Latin America Agriculture Software Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global Agriculture Software Market Revenue billion Forecast, by Deployment Type 2020 & 2033

- Table 31: Global Agriculture Software Market Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Agriculture Software Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agriculture Software Market ?

The projected CAGR is approximately 11.6%.

2. Which companies are prominent players in the Agriculture Software Market ?

Key companies in the market include Farmbrite, Deere & Company, AgJunction Inc, Topcon Corporation*List Not Exhaustive, AGCO Corporation, Conservis, AGRIVI Ltd, Oracle Corporation, Trimble Inc, Ag Leader Technology Incorporated, Raven Industries Inc.

3. What are the main segments of the Agriculture Software Market ?

The market segments include Deployment Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Penetration of the Internet in Turkey; Increase in Online Shopping; Rapid Increase in Mobile Traffic from B2C e-commerce Websites.

6. What are the notable trends driving market growth?

Platform as a Service (PaaS) to Witness the Market Growth.

7. Are there any restraints impacting market growth?

Migration of Retail Processes from On-Premise to Cloud is a Major Challenge.

8. Can you provide examples of recent developments in the market?

April 2023 - CropX, a provider of decision and planning tools, secured a Series C financing round with USD 30 million to advance its farm management system, integrating data from the earth and the sky to provide soil and crop intelligence.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agriculture Software Market ," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agriculture Software Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agriculture Software Market ?

To stay informed about further developments, trends, and reports in the Agriculture Software Market , consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence