Key Insights

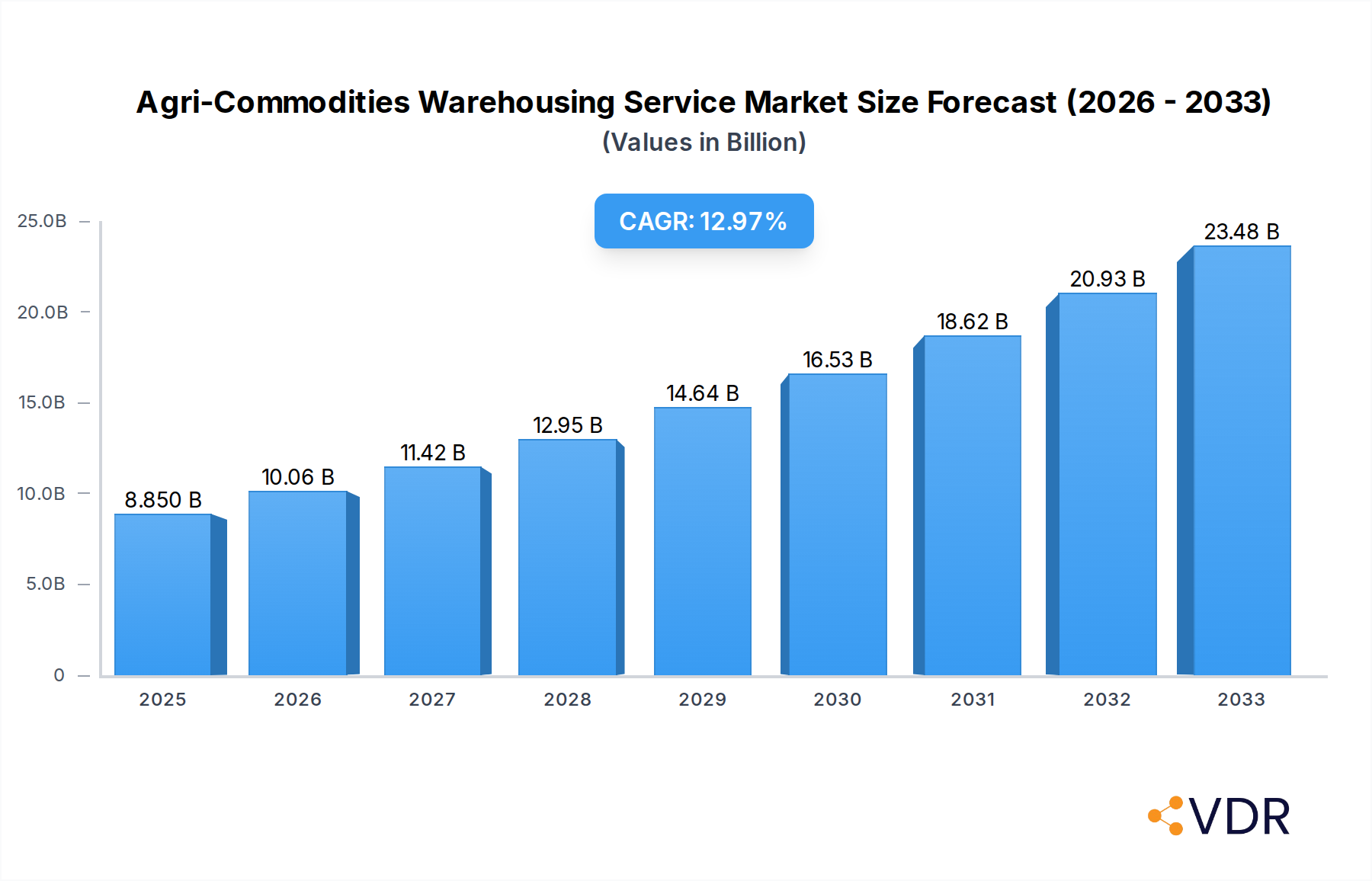

The global Agri-Commodities Warehousing Service market is poised for robust expansion, projected to reach an estimated $8.85 billion in 2025 and experience a compelling Compound Annual Growth Rate (CAGR) of 13.76% throughout the forecast period (2025-2033). This significant growth is primarily propelled by the escalating global demand for food and agricultural products, driven by a burgeoning population and evolving dietary preferences. The imperative to maintain the quality, safety, and traceability of perishable goods throughout the supply chain further fuels the need for advanced warehousing solutions. Key drivers include the increasing adoption of sophisticated cold chain logistics technologies, the expansion of e-commerce in the food sector, and government initiatives aimed at enhancing food security and reducing post-harvest losses. The market is witnessing a pronounced trend towards the development of specialized warehousing facilities equipped with advanced temperature and humidity control systems, automation, and real-time inventory management solutions to cater to the diverse needs of various agri-commodity segments.

Agri-Commodities Warehousing Service Market Size (In Billion)

The market's growth trajectory is further supported by significant investments in infrastructure development and technological innovation by major players. While the demand for warehousing services across all agri-commodity segments, including Vegetables & Fruits, Poultry, Beef and Pork, Seafood, and Dairy, is substantial, the rapidly growing demand for frozen and chilled products presents a particularly lucrative opportunity. The market is segmented into Distribution Warehouses, Public Warehouses, and Private Warehouses, with a noticeable shift towards more flexible and scalable public warehousing solutions, especially among small to medium-sized enterprises. Geographically, North America and Europe currently dominate the market due to established infrastructure and high consumer spending, but the Asia Pacific region is expected to witness the fastest growth due to its large population, increasing disposable incomes, and rapid industrialization of the agriculture sector. Despite the optimistic outlook, challenges such as the high capital investment required for state-of-the-art facilities and the need for skilled labor in specialized cold chain operations remain potential restraints.

Agri-Commodities Warehousing Service Company Market Share

Agri-Commodities Warehousing Service Market Dynamics & Structure

The global agri-commodities warehousing service market is characterized by a moderate to high degree of concentration, with key players like Lineage Logistics, Americold, and Nichirei Logistics Group holding significant market share, estimated to be collectively around 45% by value in the historical period (2019-2024). Technological innovation is a primary driver, particularly in areas like cold chain management, IoT integration for real-time monitoring, and automation in warehouse operations, leading to increased efficiency and reduced spoilage. Regulatory frameworks, including food safety standards (e.g., HACCP, GFSI) and international trade regulations, play a crucial role in shaping operational practices and market access. Competitive product substitutes, such as direct-to-consumer models and advancements in food preservation technologies, are emerging but have not significantly eroded the demand for specialized warehousing services. End-user demographics are shifting towards a greater demand for traceable and sustainably sourced food products, influencing the types of warehousing services required. Mergers and acquisitions (M&A) are an active trend, with major players acquiring smaller regional operators to expand their geographical reach and service offerings, totaling approximately 5-7 significant deals annually in recent years.

- Market Concentration: Dominated by a few large global players, with regional specialists also holding niche positions.

- Technological Innovation: Driven by cold chain advancements, IoT, and automation for efficiency.

- Regulatory Frameworks: Stringent food safety and trade regulations dictate operational standards.

- End-User Demographics: Growing demand for traceability and sustainability influencing service requirements.

- M&A Trends: Consolidation strategy to expand network and service capabilities, with an estimated deal volume of $0.5 - $1 billion annually in recent years.

Agri-Commodities Warehousing Service Growth Trends & Insights

The global agri-commodities warehousing service market is poised for robust growth, projected to expand from an estimated $150 billion in 2025 to $220 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.0%. This upward trajectory is underpinned by several critical trends. The increasing global population and rising disposable incomes in emerging economies are driving higher consumption of perishable food items, thereby escalating the demand for sophisticated warehousing solutions. Furthermore, the growing emphasis on reducing food loss and waste throughout the supply chain, driven by both economic incentives and environmental concerns, is a significant catalyst. Advanced cold chain logistics, essential for preserving the quality and extending the shelf life of perishable agri-commodities like vegetables & fruits, poultry, and dairy, are witnessing accelerated adoption rates. Technological disruptions are also playing a pivotal role, with the integration of Artificial Intelligence (AI) for inventory management and demand forecasting, alongside the widespread adoption of Internet of Things (IoT) devices for real-time temperature and humidity monitoring, enhancing operational efficiency and safety. Consumer behavior shifts are increasingly favoring products with greater transparency and traceability, compelling logistics providers to invest in advanced tracking and management systems within their warehouses. The expansion of e-commerce for groceries and fresh produce further fuels the need for specialized distribution warehouses capable of handling smaller, faster-moving orders with precision.

- Market Size Evolution: Projected to grow from $150 billion in 2025 to $220 billion by 2033.

- CAGR: Estimated at 5.0% during the forecast period (2025-2033).

- Adoption Rates: High adoption of advanced cold chain and traceability technologies.

- Technological Disruptions: AI and IoT integration for enhanced inventory management and monitoring.

- Consumer Behavior Shifts: Growing demand for transparency, traceability, and the rise of online grocery shopping.

Dominant Regions, Countries, or Segments in Agri-Commodities Warehousing Service

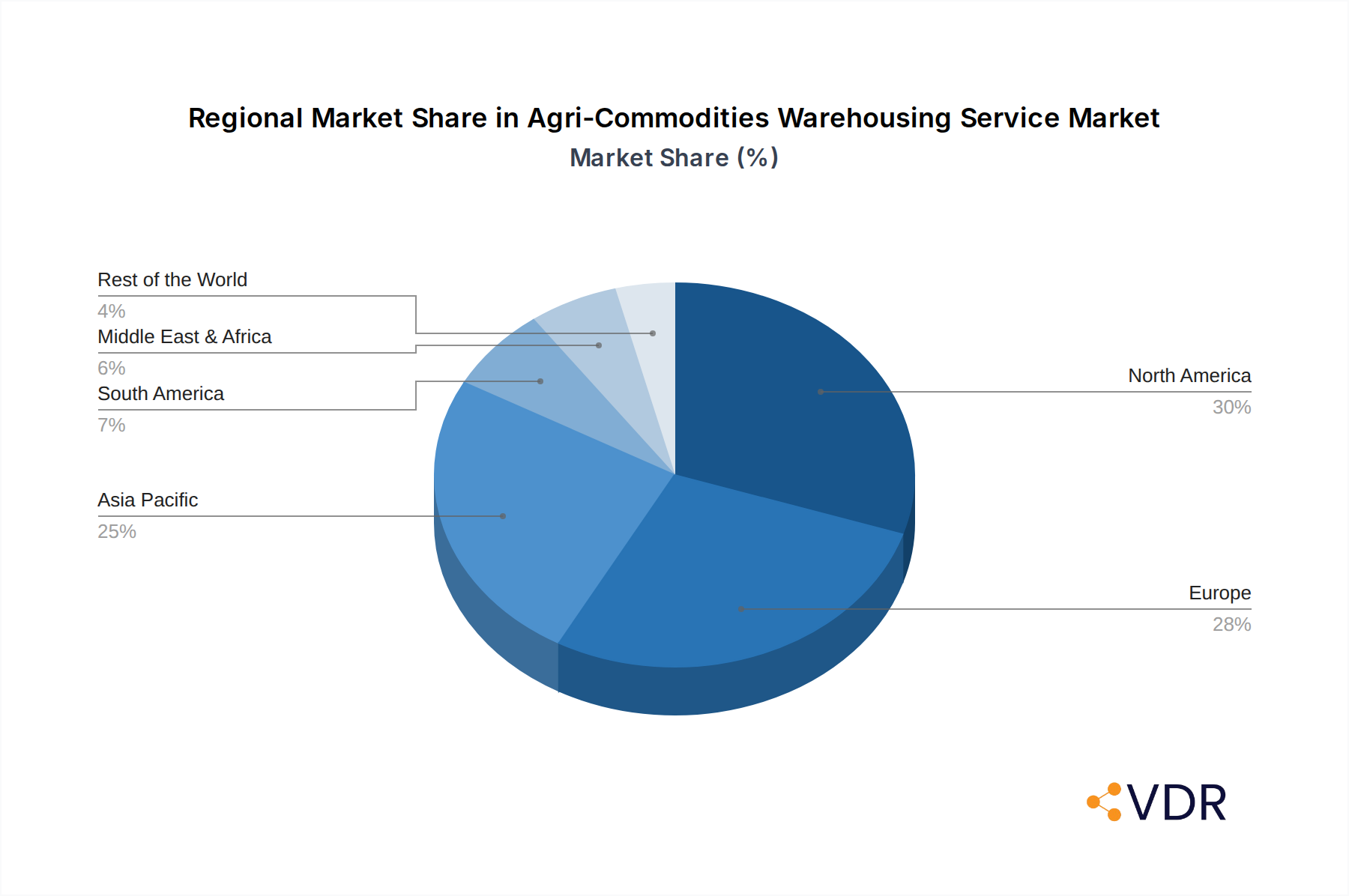

The global agri-commodities warehousing service market is experiencing dynamic shifts, with North America currently holding a dominant position, accounting for an estimated 35% of the total market value in the base year 2025. This dominance is attributed to a confluence of factors, including a highly developed agricultural sector, robust infrastructure, significant consumer demand for a wide variety of fresh and processed foods, and a mature logistics network. Within North America, the United States is the leading country, driven by its vast agricultural output and a well-established network of distribution and public warehouses catering to diverse end-user segments. The Vegetables & Fruits segment, representing approximately 25% of the total market value in 2025, is a significant growth driver, necessitating specialized temperature-controlled warehousing to maintain quality and reduce spoilage. This segment's importance is further amplified by evolving consumer preferences for fresh, healthy produce year-round.

The Types of warehouses that are crucial to this market are Distribution Warehouses and Public Warehouses. Distribution warehouses, estimated to constitute around 40% of the market in 2025, are vital for efficient product flow from producers to retailers and consumers, especially with the rise of e-commerce. Public warehouses, accounting for an estimated 35% of the market value, offer flexible storage solutions for a broad range of agri-commodities, serving a wide array of clients.

Key drivers of dominance in North America and specifically the US include:

- Economic Policies: Supportive government policies for agriculture and logistics infrastructure development.

- Infrastructure: Extensive network of roads, ports, and advanced warehousing facilities.

- Consumer Demand: High per capita consumption of perishable agri-commodities and a preference for variety.

- Technological Adoption: Early and widespread adoption of cold chain technologies and supply chain management systems.

- Market Share: The US alone accounts for over 25% of the global market value.

Looking ahead, Asia Pacific is emerging as a significant growth region, driven by increasing population, rising disposable incomes, and a growing awareness of food safety and quality. Within this region, China and India are expected to witness substantial expansion in their warehousing capacities for agri-commodities. The Poultry segment, projected at 20% of the market value in 2025, is also a key contributor due to its widespread consumption and the stringent cold chain requirements.

Agri-Commodities Warehousing Service Product Landscape

The agri-commodities warehousing service landscape is defined by specialized solutions tailored to preserve the integrity and quality of perishable goods. Innovations center on advanced temperature and humidity control systems, including multi-zone storage and blast freezing capabilities, crucial for products like Seafood and Beef and Pork. Real-time monitoring via IoT sensors, providing data on environmental conditions and product location, is a standard offering, enhancing traceability and accountability. Unique selling propositions often revolve around integrated logistics solutions, offering end-to-end supply chain management from storage to transportation. Technological advancements in warehouse automation, such as robotic picking and automated guided vehicles (AGVs), are increasingly being adopted to improve efficiency and reduce labor costs in handling high volumes of Dairy and Others (e.g., grains, processed foods).

Key Drivers, Barriers & Challenges in Agri-Commodities Warehousing Service

Key Drivers:

- Rising Global Food Demand: Increasing population necessitates efficient storage and distribution of agri-commodities.

- Technological Advancements: Innovations in cold chain, IoT, and automation enhance efficiency and reduce spoilage.

- Food Safety Regulations: Stricter compliance drives investment in modern, compliant warehousing.

- E-commerce Growth: Expansion of online grocery retail fuels demand for specialized distribution centers.

- Reduced Food Waste Initiatives: Government and industry efforts to minimize post-harvest losses.

Barriers & Challenges:

- High Capital Investment: Establishing and upgrading advanced cold chain facilities requires significant upfront capital, estimated to be in the billions of dollars for major expansions.

- Energy Costs: Maintaining precise temperature and humidity levels is energy-intensive, leading to high operational expenses.

- Skilled Labor Shortage: The need for trained personnel to operate sophisticated equipment and manage complex supply chains.

- Regulatory Compliance: Navigating diverse and evolving food safety and environmental regulations across different regions.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and transportation bottlenecks can impact service reliability.

Emerging Opportunities in Agri-Commodities Warehousing Service

Emerging opportunities lie in the growing demand for specialized warehousing for organic and sustainably produced agri-commodities, requiring adherence to specific certifications and handling protocols. The expansion of the plant-based food market presents a new segment with unique storage needs. Furthermore, the development of smart warehousing solutions integrating AI for predictive maintenance and optimized energy consumption offers significant potential for cost savings and enhanced service delivery. Untapped markets in developing regions, where cold chain infrastructure is still nascent, represent a substantial growth frontier. The increasing focus on last-mile delivery for fresh produce also opens avenues for micro-fulfillment centers integrated with warehousing hubs.

Growth Accelerators in the Agri-Commodities Warehousing Service Industry

Long-term growth in the agri-commodities warehousing service industry will be significantly accelerated by continued technological breakthroughs, particularly in areas like advanced refrigeration technologies, automation, and predictive analytics for inventory management. Strategic partnerships between warehousing providers, food producers, and retailers will foster integrated supply chain solutions, enhancing efficiency and visibility. Market expansion strategies, including mergers and acquisitions to consolidate networks and entering new geographical territories with high agricultural output and consumer demand, will be crucial. The increasing adoption of sustainable warehousing practices, such as renewable energy sources and waste reduction initiatives, will also become a key differentiator and growth accelerator, aligning with corporate ESG goals and consumer expectations.

Key Players Shaping the Agri-Commodities Warehousing Service Market

- Lineage Logistics

- Americold

- United States Cold Storage

- Nichirei Logistics Group

- VersaCold Logistics Services

- Frialsa Frigorificos

- NewCold

- Superfrio Logistica

- VX Cold Chain Logistics

- Interstate Warehousing

- Constellation Cold Logistics

- Congebec

- Sinotrans

Notable Milestones in Agri-Commodities Warehousing Service Sector

- 2019: Lineage Logistics acquires VersaCold Logistics Services, significantly expanding its North American cold chain footprint.

- 2020: Americold completes its acquisition of Cloverleaf Cold Storage, further consolidating its market position.

- 2021: Nichirei Logistics Group announces significant investments in expanding its cold storage capacity in Southeast Asia.

- 2022: NewCold opens a state-of-the-art automated cold storage facility in the United States, showcasing advanced automation.

- 2023: Constellation Cold Logistics announces strategic partnerships to enhance its temperature-controlled network across Europe.

- 2024: Sinotrans invests heavily in modernizing its cold chain logistics infrastructure to cater to China's growing agri-commodity trade.

In-Depth Agri-Commodities Warehousing Service Market Outlook

The future of the agri-commodities warehousing service market is exceptionally promising, driven by the imperative to feed a growing global population while minimizing food loss. Growth accelerators such as the increasing adoption of Industry 4.0 technologies, including AI-powered demand forecasting and robotic automation, will lead to unprecedented levels of operational efficiency. Strategic market expansions into high-growth regions in Asia Pacific and Africa will unlock new revenue streams. The ongoing evolution of consumer preferences towards healthier, traceable, and sustainably produced food will continue to shape the demand for specialized, value-added warehousing services. The market is poised for sustained expansion, offering significant strategic opportunities for innovation and investment in a sector critical to global food security and sustainability.

Agri-Commodities Warehousing Service Segmentation

-

1. Application

- 1.1. Vegetables & Fruits

- 1.2. Poultry, Beef and Pork

- 1.3. Seafood

- 1.4. Dairy

- 1.5. Others

-

2. Types

- 2.1. Distribution Warehouse

- 2.2. Public Warehouse

- 2.3. Private Warehouse

Agri-Commodities Warehousing Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Agri-Commodities Warehousing Service Regional Market Share

Geographic Coverage of Agri-Commodities Warehousing Service

Agri-Commodities Warehousing Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.76% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Vegetables & Fruits

- 5.1.2. Poultry, Beef and Pork

- 5.1.3. Seafood

- 5.1.4. Dairy

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Distribution Warehouse

- 5.2.2. Public Warehouse

- 5.2.3. Private Warehouse

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Vegetables & Fruits

- 6.1.2. Poultry, Beef and Pork

- 6.1.3. Seafood

- 6.1.4. Dairy

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Distribution Warehouse

- 6.2.2. Public Warehouse

- 6.2.3. Private Warehouse

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Vegetables & Fruits

- 7.1.2. Poultry, Beef and Pork

- 7.1.3. Seafood

- 7.1.4. Dairy

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Distribution Warehouse

- 7.2.2. Public Warehouse

- 7.2.3. Private Warehouse

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Vegetables & Fruits

- 8.1.2. Poultry, Beef and Pork

- 8.1.3. Seafood

- 8.1.4. Dairy

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Distribution Warehouse

- 8.2.2. Public Warehouse

- 8.2.3. Private Warehouse

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Vegetables & Fruits

- 9.1.2. Poultry, Beef and Pork

- 9.1.3. Seafood

- 9.1.4. Dairy

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Distribution Warehouse

- 9.2.2. Public Warehouse

- 9.2.3. Private Warehouse

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Agri-Commodities Warehousing Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Vegetables & Fruits

- 10.1.2. Poultry, Beef and Pork

- 10.1.3. Seafood

- 10.1.4. Dairy

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Distribution Warehouse

- 10.2.2. Public Warehouse

- 10.2.3. Private Warehouse

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Lineage Logistics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Americold

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 United States Cold Storage

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nichirei Logistics Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 VersaCold Logistics Services

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Frialsa Frigorificos

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 NewCold

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Superfrio Logistica

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 VX Cold Chain Logistics

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Interstate Warehousing

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Constellation Cold Logistics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Congebec

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sinotrans

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Lineage Logistics

List of Figures

- Figure 1: Global Agri-Commodities Warehousing Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Agri-Commodities Warehousing Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Agri-Commodities Warehousing Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Agri-Commodities Warehousing Service Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Agri-Commodities Warehousing Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Agri-Commodities Warehousing Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Agri-Commodities Warehousing Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Agri-Commodities Warehousing Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Agri-Commodities Warehousing Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Agri-Commodities Warehousing Service Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Agri-Commodities Warehousing Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Agri-Commodities Warehousing Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Agri-Commodities Warehousing Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Agri-Commodities Warehousing Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Agri-Commodities Warehousing Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Agri-Commodities Warehousing Service Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Agri-Commodities Warehousing Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Agri-Commodities Warehousing Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Agri-Commodities Warehousing Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Agri-Commodities Warehousing Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Agri-Commodities Warehousing Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Agri-Commodities Warehousing Service Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Agri-Commodities Warehousing Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Agri-Commodities Warehousing Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Agri-Commodities Warehousing Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Agri-Commodities Warehousing Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Agri-Commodities Warehousing Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Agri-Commodities Warehousing Service Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Agri-Commodities Warehousing Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Agri-Commodities Warehousing Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Agri-Commodities Warehousing Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Agri-Commodities Warehousing Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Agri-Commodities Warehousing Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Agri-Commodities Warehousing Service?

The projected CAGR is approximately 13.76%.

2. Which companies are prominent players in the Agri-Commodities Warehousing Service?

Key companies in the market include Lineage Logistics, Americold, United States Cold Storage, Nichirei Logistics Group, VersaCold Logistics Services, Frialsa Frigorificos, NewCold, Superfrio Logistica, VX Cold Chain Logistics, Interstate Warehousing, Constellation Cold Logistics, Congebec, Sinotrans.

3. What are the main segments of the Agri-Commodities Warehousing Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.85 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Agri-Commodities Warehousing Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Agri-Commodities Warehousing Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Agri-Commodities Warehousing Service?

To stay informed about further developments, trends, and reports in the Agri-Commodities Warehousing Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence