Key Insights

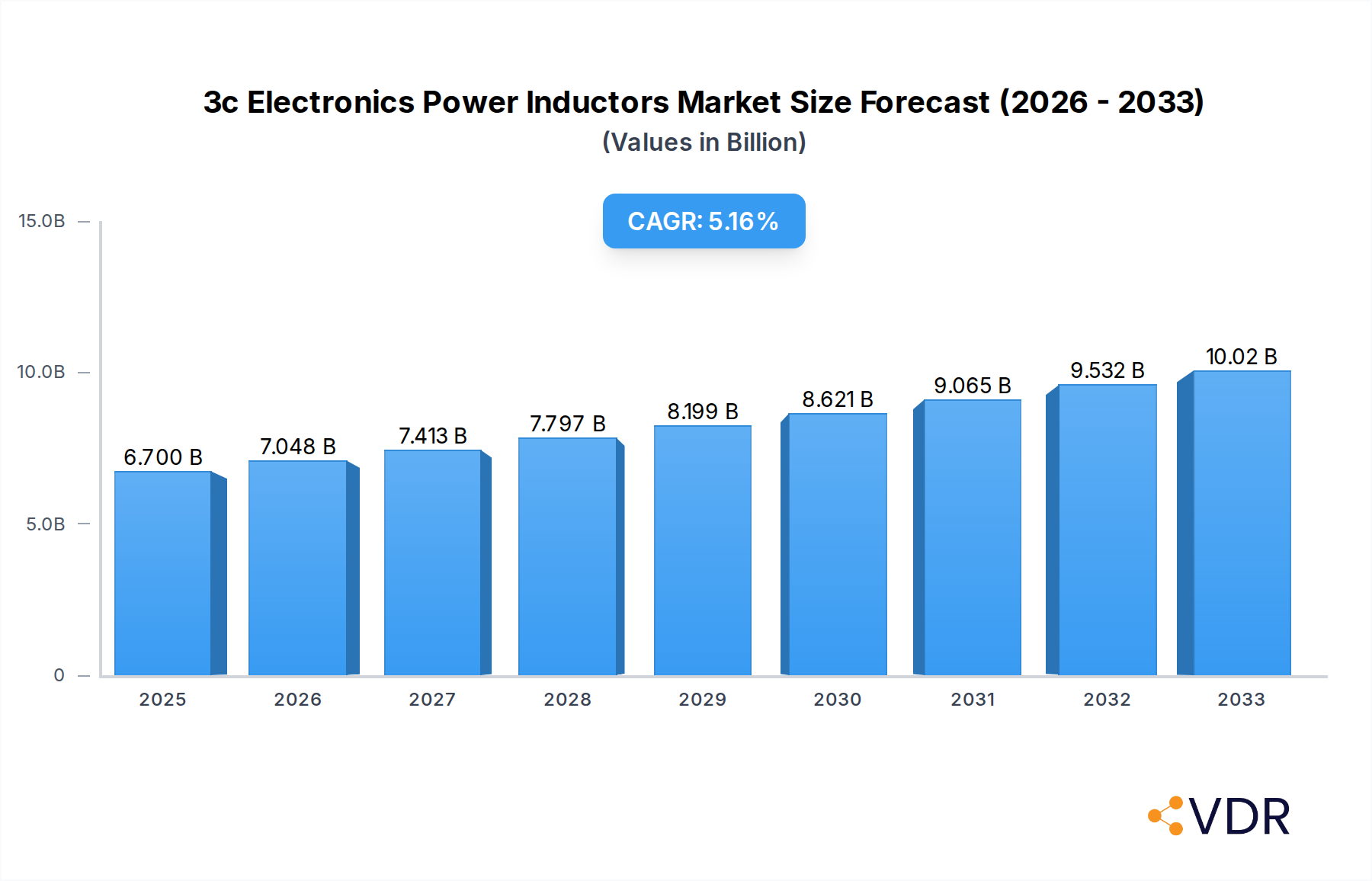

The 3C Electronics Power Inductors market is poised for robust expansion, projected to reach a substantial $6.7 billion by 2025. This growth is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 5.3% anticipated over the forecast period of 2025-2033. The market is primarily driven by the insatiable demand for miniaturization and enhanced power efficiency across a wide spectrum of electronic devices. The proliferation of smartphones, wearables, and advanced computing systems necessitates smaller, more powerful inductors capable of handling increased current densities and operating at higher frequencies. Furthermore, the burgeoning Internet of Things (IoT) ecosystem, with its myriad connected devices, contributes significantly to this upward trajectory. Emerging trends such as the integration of power inductors into advanced packaging solutions and the increasing adoption of wireless charging technologies are also shaping market dynamics. These advancements enable more compact and efficient electronic designs, pushing the boundaries of technological innovation.

3c Electronics Power Inductors Market Size (In Billion)

Despite the optimistic outlook, certain restraints could influence the market's pace. The rising cost of raw materials, particularly specialty metals and rare earth elements used in inductor manufacturing, may pose a challenge. Additionally, the complex manufacturing processes and the need for specialized expertise can create barriers to entry for new players. However, the market's segmentation reveals strong potential in both Computer Electronics and Consumer Electronics applications, with SMD Power Inductors leading in adoption due to their surface-mount capabilities and suitability for automated assembly. The continuous evolution of semiconductor technology and the increasing complexity of power management circuits within these electronics are expected to sustain demand. Key players like TDK, Murata, and Vishay are at the forefront, investing in research and development to deliver innovative solutions that address these evolving market needs and overcome potential challenges.

3c Electronics Power Inductors Company Market Share

3c Electronics Power Inductors Market Dynamics & Structure

The global 3c electronics power inductors market is characterized by a moderate to high level of concentration, with established players like TDK, Murata, Vishay, and Taiyo Yuden holding significant market shares. Technological innovation remains a primary driver, fueled by the relentless demand for miniaturization, higher efficiency, and advanced functionalities in electronic devices. Regulatory frameworks, particularly those related to environmental compliance (e.g., RoHS, REACH) and electromagnetic interference (EMI) standards, are increasingly shaping product development and market access. Competitive product substitutes, while limited in the core function of power inductors, can emerge in integrated solutions or alternative power management architectures. End-user demographics are diverse, spanning professionals in computer electronics, communication electronics, and consumer electronics, each with distinct performance and cost requirements. Mergers and acquisitions (M&A) activity, though not always high volume, often targets companies with specialized technological capabilities or strong regional footholds. For instance, the acquisition of smaller, innovative inductor manufacturers by larger component suppliers aims to broaden product portfolios and expand market reach. The market is anticipated to see an increase in the volume of M&A deals focused on niche technologies and specialized application areas as the parent and child markets mature.

- Market Concentration: Moderate to High. Key players include TDK, Murata, Vishay, Taiyo Yuden, Sagami Elec, Sumida, Chilisin, Mitsumi Electric, Shenzhen Microgate Technology, Delta Electronics, Sunlord Electronics, Panasonic, AVX (Kyocera), API Delevan, Würth Elektronik, Littelfuse, Pulse Electronics, Coilcraft, Inc, Ice Components.

- Technological Innovation Drivers: Miniaturization, increased power density, higher efficiency, wider operating temperature ranges, and advanced materials.

- Regulatory Frameworks: RoHS, REACH, FCC, CE certifications, and evolving energy efficiency standards.

- Competitive Product Substitutes: Integrated power modules, advanced DC-DC converters with fewer discrete components.

- End-User Demographics: Professionals in computer electronics (e.g., laptops, desktops), communication electronics (e.g., smartphones, base stations), and consumer electronics (e.g., wearables, smart home devices).

- M&A Trends: Strategic acquisitions of companies with niche technologies or strong regional presence. Anticipated increase in deal volume in specialized segments.

3c Electronics Power Inductors Growth Trends & Insights

The global 3c electronics power inductors market is poised for robust growth, driven by the pervasive digitalization across industries and the insatiable demand for advanced electronic devices. The market size, valued at approximately 3.5 billion units in 2024, is projected to expand at a Compound Annual Growth Rate (CAGR) of 5.2% from 2025 to 2033, reaching an estimated 5.4 billion units by the end of the forecast period. This expansion is underpinned by several key trends. The relentless evolution of computing devices, from ultra-portable laptops to high-performance servers, necessitates increasingly sophisticated and compact power management solutions, directly benefiting the power inductor sector. In the realm of communication electronics, the rollout of 5G infrastructure, the proliferation of IoT devices, and the ever-increasing bandwidth requirements in smartphones are creating sustained demand for high-frequency and high-efficiency power inductors. Consumer electronics, while subject to cyclical trends, continues to innovate with wearable technology, smart home ecosystems, and advanced audio-visual equipment, all of which integrate power inductors. Adoption rates are steadily increasing, driven by the need to meet stringent energy efficiency mandates and reduce the physical footprint of electronic components. Technological disruptions, such as the development of novel magnetic materials and advanced manufacturing techniques, are enabling the production of smaller, more powerful, and more reliable inductors. Consumer behavior shifts towards devices with longer battery life, faster charging capabilities, and enhanced performance further amplify the demand for efficient power management components. The parent market, encompassing all passive components in electronics, provides a broad context for the growth of power inductors, while specialized child markets, such as those for automotive or industrial power inductors, present distinct yet interconnected growth trajectories. The increasing integration of artificial intelligence and machine learning in electronic devices also indirectly fuels demand by requiring more computational power and, consequently, more robust power delivery.

Dominant Regions, Countries, or Segments in 3c Electronics Power Inductors

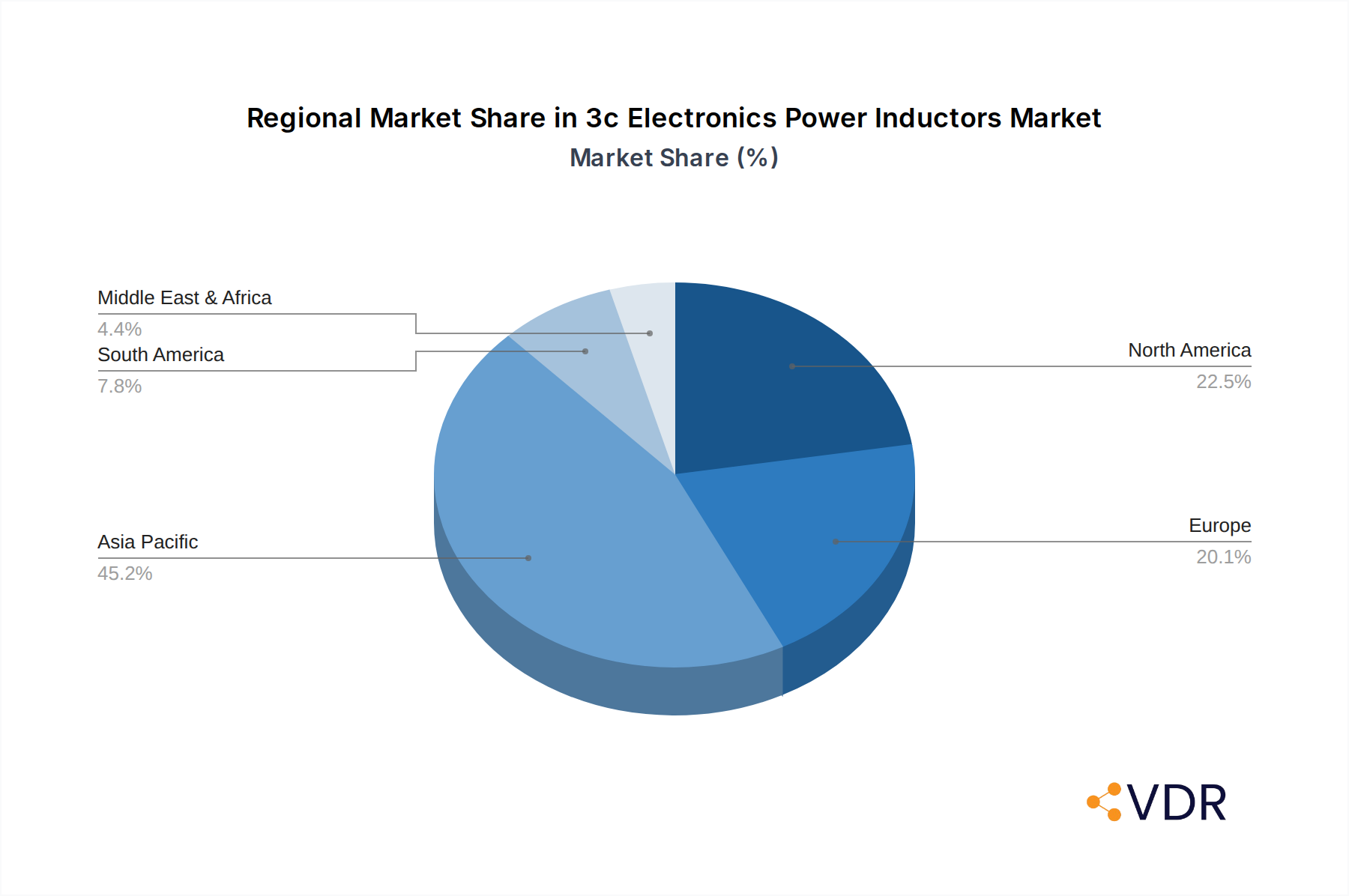

Within the dynamic landscape of the 3c electronics power inductors market, Asia Pacific stands out as the dominant region, driven by its entrenched position as the global manufacturing hub for electronics. Countries like China, South Korea, Japan, and Taiwan are at the forefront of this dominance, fueled by substantial government support for the electronics industry, a vast and skilled labor force, and the presence of major original design manufacturers (ODMs) and original equipment manufacturers (OEMs). The sheer volume of production for computer electronics, communication electronics, and consumer electronics originating from this region directly translates into a massive demand for power inductors. For example, China alone accounts for a significant portion of global electronics manufacturing, and its internal demand for power inductors is colossal, supported by government initiatives focused on technological self-sufficiency and the growth of its domestic technology giants.

In terms of segments, SMD Power Inductors are the primary growth driver, owing to their widespread adoption in space-constrained modern electronic devices. The trend towards miniaturization in smartphones, tablets, laptops, and wearable technology makes Surface Mount Device (SMD) inductors indispensable. Their automated assembly compatibility further enhances their appeal for mass production. The market share of SMD power inductors is estimated to be around 75% of the total 3c electronics power inductors market in 2025, with a projected growth rate exceeding that of plug-in variants.

Key drivers for Asia Pacific's dominance include:

- Manufacturing Ecosystem: The presence of a complete electronics manufacturing supply chain, from component fabrication to final assembly.

- Economic Policies: Favorable government policies promoting electronics manufacturing, R&D, and export.

- Infrastructure Development: Robust logistics and transportation networks facilitating global trade.

- Growing Domestic Demand: An expanding middle class and increasing per capita income driving consumer electronics consumption.

- Technological Advancement: Significant investments in R&D by local companies leading to innovation in inductor technology.

Within the application segment, Computer Electronics and Communication Electronics are key contributors to the market's growth, often overlapping in their demand for advanced power solutions. The continuous upgrade cycles for personal computers, the expansion of data centers, and the relentless evolution of mobile communication technologies all necessitate high-performance power inductors. The market share for computer electronics is estimated at 30%, while communication electronics accounts for approximately 35% in 2025. Consumer electronics, while substantial, exhibits more seasonal demand fluctuations.

3c Electronics Power Inductors Product Landscape

The 3c electronics power inductors product landscape is defined by ongoing innovation in materials science and manufacturing processes, leading to devices with superior performance characteristics. Key product advancements include the development of power inductors with higher current handling capabilities in smaller form factors, crucial for power-dense applications in modern computing and communication devices. Innovations in magnetic core materials, such as advanced ferrites and composite materials, enable reduced core losses, leading to increased energy efficiency and extended battery life in portable electronics. Furthermore, the demand for higher operating frequencies has spurred the development of power inductors with lower parasitic capacitance and improved high-frequency response, essential for advanced wireless communication systems. These product innovations directly address the evolving needs of the parent market for miniaturization and enhanced functionality, while catering to the specific requirements of child markets like automotive electronics, which demand ruggedness and wide operating temperature ranges.

Key Drivers, Barriers & Challenges in 3c Electronics Power Inductors

Key Drivers:

- Miniaturization Demand: The persistent need for smaller and lighter electronic devices across all 3c segments, from smartphones to IoT devices, is a primary growth engine.

- Increasing Power Efficiency Requirements: Stringent energy regulations and consumer demand for longer battery life are pushing for more efficient power management solutions, where inductors play a critical role.

- 5G and IoT Expansion: The widespread deployment of 5G networks and the burgeoning Internet of Things ecosystem require sophisticated power solutions, driving demand for advanced power inductors.

- Technological Advancements in Materials: Innovations in magnetic materials and manufacturing techniques enable higher performance in smaller form factors.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the prices of key raw materials like copper and rare earth elements can impact manufacturing costs and profit margins.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and trade disputes can lead to supply chain vulnerabilities, affecting component availability and lead times.

- Intense Competition and Price Pressures: The mature nature of some segments leads to aggressive competition and pressure on pricing, particularly for standard components.

- Technological Obsolescence: Rapid technological advancements can render older inductor designs obsolete, requiring continuous investment in R&D.

Emerging Opportunities in 3c Electronics Power Inductors

Emerging opportunities in the 3c electronics power inductors sector are largely driven by the expansion of cutting-edge technologies and evolving consumer preferences. The burgeoning electric vehicle (EV) market, a significant child market, presents a substantial opportunity for high-power, high-reliability inductors used in onboard charging systems, motor controllers, and DC-DC converters. Furthermore, the ongoing development of smart grid technologies and renewable energy systems necessitates specialized inductors for power conversion and energy storage. The increasing adoption of AI-powered devices and edge computing demands more power-efficient and compact components, creating a niche for advanced inductors with superior thermal management capabilities. The growth of the metaverse and augmented/virtual reality (AR/VR) devices also signifies a future demand for highly integrated and miniaturized power solutions.

Growth Accelerators in the 3c Electronics Power Inductors Industry

Several factors are acting as significant growth accelerators for the 3c electronics power inductors industry. The continuous innovation in semiconductor technology, leading to higher switching frequencies and power densities in integrated circuits, directly necessitates complementary advancements in power inductors to maintain efficiency and form factor miniaturization. Strategic partnerships between inductor manufacturers and leading semiconductor companies, for instance, can expedite the co-development of optimized power management solutions, ensuring seamless integration and superior performance. Furthermore, market expansion strategies focusing on emerging economies and their rapidly growing electronics sectors, coupled with increasing localized manufacturing capabilities, will broaden the industry's reach and drive sales volume. The relentless pursuit of higher energy efficiency standards by governments worldwide also acts as a potent accelerator, compelling manufacturers to invest in and develop more advanced inductor technologies.

Key Players Shaping the 3c Electronics Power Inductors Market

- TDK

- Murata

- Vishay

- Taiyo Yuden

- Sagami Elec

- Sumida

- Chilisin

- Mitsumi Electric

- Shenzhen Microgate Technology

- Delta Electronics

- Sunlord Electronics

- Panasonic

- AVX (Kyocera)

- API Delevan

- Würth Elektronik

- Littelfuse

- Pulse Electronics

- Coilcraft, Inc

- Ice Components

Notable Milestones in 3c Electronics Power Inductors Sector

- 2019: Introduction of advanced composite core materials enabling higher current density in SMD power inductors.

- 2020: Significant increase in demand for high-frequency inductors driven by the initial rollout of 5G infrastructure globally.

- 2021: Major manufacturers announce increased production capacity to meet the burgeoning demand from the consumer electronics sector, recovering from pandemic-related disruptions.

- 2022: Focus on sustainable manufacturing practices and eco-friendly materials gains traction among leading players.

- 2023: Introduction of novel inductor designs with integrated shielding for enhanced electromagnetic interference (EMI) reduction in sensitive applications.

- 2024 (Early): Enhanced R&D investments in high-temperature tolerant power inductors for automotive and industrial applications.

In-Depth 3c Electronics Power Inductors Market Outlook

The outlook for the 3c electronics power inductors market is exceptionally positive, driven by the persistent technological evolution across the parent and child markets. The forecast period from 2025 to 2033 is expected to witness sustained growth, fueled by the increasing ubiquity of connected devices, the electrification of transportation, and the ongoing digital transformation of industries. Strategic opportunities lie in developing highly integrated, miniaturized power solutions for the next generation of smartphones, wearables, and AR/VR devices. The automotive sector, particularly electric vehicles, represents a significant growth accelerator due to the demand for robust and high-performance power inductors. Continued investment in advanced materials and manufacturing processes will be crucial for manufacturers to maintain a competitive edge and capitalize on these expanding market frontiers.

3c Electronics Power Inductors Segmentation

-

1. Application

- 1.1. Computer Electronics

- 1.2. Communication Electronics

- 1.3. Consumer Electronics

-

2. Type

- 2.1. SMD Power Inductors

- 2.2. Plug-in Power Inductors

3c Electronics Power Inductors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

3c Electronics Power Inductors Regional Market Share

Geographic Coverage of 3c Electronics Power Inductors

3c Electronics Power Inductors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Computer Electronics

- 5.1.2. Communication Electronics

- 5.1.3. Consumer Electronics

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. SMD Power Inductors

- 5.2.2. Plug-in Power Inductors

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Computer Electronics

- 6.1.2. Communication Electronics

- 6.1.3. Consumer Electronics

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. SMD Power Inductors

- 6.2.2. Plug-in Power Inductors

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Computer Electronics

- 7.1.2. Communication Electronics

- 7.1.3. Consumer Electronics

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. SMD Power Inductors

- 7.2.2. Plug-in Power Inductors

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Computer Electronics

- 8.1.2. Communication Electronics

- 8.1.3. Consumer Electronics

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. SMD Power Inductors

- 8.2.2. Plug-in Power Inductors

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Computer Electronics

- 9.1.2. Communication Electronics

- 9.1.3. Consumer Electronics

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. SMD Power Inductors

- 9.2.2. Plug-in Power Inductors

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific 3c Electronics Power Inductors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Computer Electronics

- 10.1.2. Communication Electronics

- 10.1.3. Consumer Electronics

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. SMD Power Inductors

- 10.2.2. Plug-in Power Inductors

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 TDK

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Murata

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Vishay

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Taiyo Yuden

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sagami Elec

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sumida

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Chilisin

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mitsumi Electric

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shenzhen Microgate Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Delta Electronics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sunlord Electronics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Panasonic

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 AVX (Kyocera)

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 API Delevan

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Würth Elektronik

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Littelfuse

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Pulse Electronics

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Coilcraft Inc

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Ice Components

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 TDK

List of Figures

- Figure 1: Global 3c Electronics Power Inductors Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America 3c Electronics Power Inductors Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America 3c Electronics Power Inductors Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America 3c Electronics Power Inductors Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America 3c Electronics Power Inductors Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America 3c Electronics Power Inductors Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America 3c Electronics Power Inductors Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America 3c Electronics Power Inductors Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America 3c Electronics Power Inductors Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America 3c Electronics Power Inductors Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America 3c Electronics Power Inductors Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America 3c Electronics Power Inductors Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America 3c Electronics Power Inductors Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe 3c Electronics Power Inductors Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe 3c Electronics Power Inductors Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe 3c Electronics Power Inductors Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe 3c Electronics Power Inductors Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe 3c Electronics Power Inductors Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe 3c Electronics Power Inductors Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa 3c Electronics Power Inductors Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa 3c Electronics Power Inductors Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa 3c Electronics Power Inductors Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa 3c Electronics Power Inductors Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa 3c Electronics Power Inductors Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa 3c Electronics Power Inductors Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific 3c Electronics Power Inductors Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific 3c Electronics Power Inductors Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific 3c Electronics Power Inductors Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific 3c Electronics Power Inductors Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific 3c Electronics Power Inductors Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific 3c Electronics Power Inductors Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global 3c Electronics Power Inductors Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific 3c Electronics Power Inductors Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3c Electronics Power Inductors?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the 3c Electronics Power Inductors?

Key companies in the market include TDK, Murata, Vishay, Taiyo Yuden, Sagami Elec, Sumida, Chilisin, Mitsumi Electric, Shenzhen Microgate Technology, Delta Electronics, Sunlord Electronics, Panasonic, AVX (Kyocera), API Delevan, Würth Elektronik, Littelfuse, Pulse Electronics, Coilcraft, Inc, Ice Components.

3. What are the main segments of the 3c Electronics Power Inductors?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3c Electronics Power Inductors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3c Electronics Power Inductors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3c Electronics Power Inductors?

To stay informed about further developments, trends, and reports in the 3c Electronics Power Inductors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence